Key Takeaways

- Out-of-state real estate investing is worth it when you have the right market, the right operator on the ground, the right strategy for that market, and the cash reserves to absorb a bad year — and not worth it when any one of those is missing

- I’ve done 24 deals across NC, OH, SC, and TX since 2020. Five of them were a Cleveland cluster I eventually exited; the other 19 are why I’m still doing this

- The Cleveland properties looked good on paper. The numbers ran. The “perfect BRRRR” hit its appraisal. None of that was the problem

- The cost of being wrong about a market is usually a year or two of your life and tens of thousands of dollars per property — not catastrophic, not zero either

- Out-of-state investing is a leverage multiplier. It magnifies a good system and it magnifies a bad one. The work is on the system, not the geography

IN THIS ARTICLE

- The Question Everyone Asks Wrong

- What “Out-of-State” Actually Means

- The Cleveland Story: When OOS Investing Doesn’t Work

- What “Worth It” Actually Looks Like: The North Carolina System

- When OOS Investing Is Worth It (And When It Isn’t)

- What Most People Get Wrong About OOS Investing

- How This Changes If You’re Investing From Outside the US

- Frequently Asked Questions

The Question Everyone Asks Wrong

Most people asking “is out-of-state real estate investing worth it” are asking the wrong question. The honest version is: worth it for whom, in what market, with what team, on what strategy? Change any of those four variables and the answer flips.

I’ve done 24 deals over six years across four states. I built a US real estate portfolio while living in Israel — never in the same time zone as any of my properties, almost never on the ground for a closing. Most of what I own I have never physically visited. The portfolio works. It also includes five properties in Cleveland that I spent four years quietly exiting because they were the wrong properties in the wrong market with the wrong system behind them.

So when someone asks me whether out-of-state investing is worth it, I don’t say yes. I don’t say no. I say: it’s worth it when these specific things are in place. It’s not worth it when they aren’t. Most of the blog posts ranking for this question are written by people who have not had to make this trade-off with their own capital. This one is.

What “Out-of-State” Actually Means (And Why I’m the Wrong Person and the Right Person to Answer This)

Out-of-state investing is investing in a market you don’t live in and can’t drive to in an afternoon. That’s the whole definition. The investor in Los Angeles buying in Cleveland is doing OOS investing. So is the investor in Tel Aviv doing the same. The friction is identical: you can’t see the property, you don’t know the streets, you can’t be at the closing, you can’t meet the property manager in person without buying a plane ticket.

I’m the wrong person to answer this if you want a US-domestic-investor perspective. I’ve never done a deal in a market I could drive to. I’m the right person to answer it because the friction that domestic OOS investors hit — bad PMs, market misreads, contractor delays you can’t supervise — I hit harder, with a 7-hour time difference and a foreign passport on top. If a system works for me, it works for the investor in California buying in Indianapolis. The opposite isn’t always true.

The other thing worth saying upfront: I’m not selling a course. I don’t run a turnkey company. I’m not going to tell you “yes it’s worth it, click here to buy my masterclass.” The blogs that say it’s always worth it tend to be the ones with something to sell you. Read them with that in mind.

The Cleveland Story: What It Looks Like When OOS Investing Doesn’t Work

In 2021 I bought five single-family BRRRRs in Cleveland. Three solo, two with a partner. The setup made sense to me at the time: low entry prices ($80k–$93k purchase, $20k–$24k rehabs), strong rent-to-price ratios on paper, projected appraisals at $116k–$146k, projected cash flow around $300–$350 per door. On a spreadsheet it looked like a portfolio. I was 18 months into investing, my Fayetteville BRRRR had worked, and I wanted to scale.

Here’s what actually happened over the next four years. The tenants in the first three properties cycled through in patterns I didn’t have language for at the time — late rent, mid-lease departures, units returned with damage that ate the year’s cash flow. Maintenance bills came in on a schedule that turned $300/month cash flow into break-even. The property manager I’d hired was reactive, not proactive — fine when nothing was wrong, useless when something was. By the time I had enough data to know the system wasn’t working, I was already deep into year two.

The fourth deal — the one I called “the perfect BRRRR” — had numbers that worked even in this market. $88k purchase, only $6k rehab, $146k appraisal, $350/month cash flow projected. That was the deal that taught me the real lesson. Even with the math right, the market was still wrong. Tenant quality, neighborhood trajectory, and exit liquidity weren’t on my spreadsheet, and they were the things that actually decided the outcome.

Between 2023 and 2026 I sold all five. Some at small losses, some at break-even, the partnership deals at modest profit but only because we held them long enough for the market to catch up to where we’d bought. Across the cluster I tied up real capital for several years that should have been compounding in better markets. That’s the cost. Not catastrophic. Not zero either. The kind of mistake that’s expensive enough to remember and survivable enough to learn from.

What I’d do differently is not “pick a different market.” It’s the layer underneath that. I’d spend three months on the ground in any new market — visiting twice, walking neighborhoods, interviewing three PMs and three contractors — before deploying real capital. I’d buy one property and hold it through one full tenant cycle (12–18 months) before buying the next. The Cleveland cluster failed because I bought five properties with the diligence appropriate for one.

What “Worth It” Actually Looks Like: The North Carolina System

The other 19 deals are why I’m still doing this. The center of gravity is North Carolina — Fayetteville, Winston-Salem, Newton, Hickory, Kings Mountain, Thomasville, Gastonia, Durham. One builder I work with on most of the new construction. One or two PMs per submarket. A real estate agent who sources off-market deals before they hit the MLS. I make decisions on properties I’ve never seen because the people who have seen them have my trust — earned over years, not assumed on day one.

The numbers in this part of the portfolio: my first BRRRR in Fayetteville (2021) — $102k purchase + $18k rehab → $165k appraisal, pulled all the cash out, still cash flows $350/month. My Kings Mountain BRRRR (2022) — $100k + $30k → $175k appraisal, 100% other people’s money, $500/month cash flow. The Newton duplex (2024) — $135k + $100k → $275k appraisal, $450/month cash flow, plus an adjacent development lot that came with the deal at no additional cost. Two creative-finance deals in Columbia SC and San Antonio TX in 2026 — $30k and $32k of my own money into $280k assets, both cash-flowing $400/month.

None of these worked because I’m a better investor than I was in 2021. They worked because the system around them is different. The market is one I’ve been in for years. The team has institutional memory of what does and doesn’t work. When my builder calls to say a deal is on the table, I trust the call because I’ve seen him be right hundreds of times. The framework I built around this — capital allocation, market selection, team management — is what I walk through in the building a US real estate portfolio from Israel breakdown for anyone who wants the full sequence.

The cash flow side has finally arrived (~$2,300/month from active rentals as of 2026), but the engine that produced it was equity, not cash flow. Every property bought below market, rehabbed correctly, refinanced based on appraisal, has compounded equity that I keep redeploying. That’s the model that works for OOS investors with patience. The “$5k/month passive income in 12 months” model that dominates the YouTube algorithm — that’s not what’s worked for me.

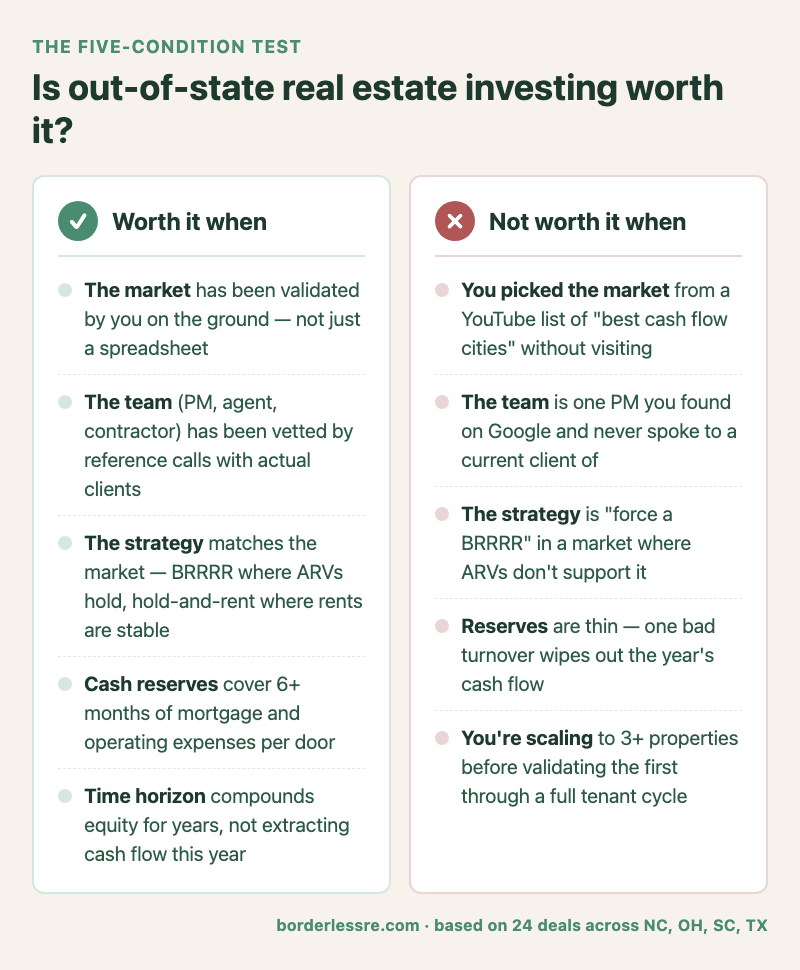

When Out-of-State Investing Is Worth It (And When It Isn’t)

The honest answer to the question is conditional. Below is the framework I’d hand to someone deciding whether to do this.

The pattern is consistent across my own deals and across every OOS investor I’ve watched succeed or fail. The investors who win at OOS investing aren’t the ones who picked the cleverest market — they’re the ones who built the system before they scaled. The investors who fail aren’t unintelligent or unlucky. They scaled before validating, or they trusted a number on a spreadsheet over a person on the ground.

If you’re a beginner asking out of state real estate investing for beginners, the most useful thing I can tell you is: pick one market, build a real team there over 6–12 months, and buy one property. Hold it through one full tenant cycle. Watch how your team responds when something goes wrong (it will). Only then think about a second property. The investors who treat their first OOS deal as a test of the system rather than the start of a portfolio are the ones who go on to build portfolios.

What Most People Get Wrong About Out-of-State Investing

The conventional wisdom on this topic is mostly bad. Three things, in order of how much they cost.

Mistake #1: Treating market selection as the most important decision. It isn’t. Team selection is. A good team in a B-market beats a great market with a bad team every single time. Cleveland is a perfectly viable market for some investors today. It wasn’t viable for me in 2021 because the team I assembled couldn’t compensate for my distance. The Reddit shorthand “out-of-state investing is dangerous” is wrong about the cause — the danger is rarely the geography. It’s the thinness of the team holding the geography together.

Mistake #2: Believing cash flow projections from a spreadsheet. Every property I’ve ever bought projected positive cash flow on the analyzer. About half of them actually delivered it in year one. Maintenance reserves get hit, vacancies happen, evictions happen, capex events happen. The realistic operating margin on a single-family rental is much thinner than the BiggerPockets calculator suggests. If your deal only works at the projected number, it doesn’t really work. Build in a buffer of at least 30% on operating expenses before you call a deal a winner.

Mistake #3: Treating OOS investing as a way to start. It’s a way to scale, not a way to start. The investors who do OOS as their first-ever real estate purchase have a much higher failure rate than the investors who did one local deal first to learn the operational reality. If you’ve never been a landlord, never managed a turnover, never coordinated a contractor — adding 1,500 miles of distance to your first try is harder than it needs to be. The exception is investors with no viable local market (this is most foreign investors, including me — Israel doesn’t have a real OOS-equivalent market for non-citizens) and they get the rougher learning curve as a structural condition. If you have a viable local market and you’re choosing OOS for “better numbers,” consider local first.

The point that earns the link in this category: the question is not “is OOS worth it” — it’s “do I have the discipline to build the system before I deploy the capital?” That’s the entire game.

How This Changes If You’re Investing From Outside the US

If you’re a foreign investor reading this — same friction, multiplied. The market diligence work is the same. The team-building work is the same. The discipline of buying one and holding it through a cycle before scaling is the same. The added layers are: financing (you’ll need a DSCR loan instead of a conventional mortgage), entity setup (an LLC for liability and operations), tax structure (FIRPTA on exit, which has its own playbook), and the operational reality of doing wires across borders and signing closings via DocuSign at 2am local time.

None of that changes the underlying answer. It changes the time-and-money cost of the setup phase. The Israel-based investor doing this for the first time should expect 3–6 months of preparation work before they’re ready to make an offer. The full setup walkthrough lives in how to invest in US real estate from abroad. The financing piece is in BRRRR for foreign nationals.

For the international investor, the question becomes more conditional, not less. The setup cost is higher. The first-deal stakes are higher because you can’t easily turn around and go look at the property in person if something starts going wrong. But the upside is also more meaningful because the alternative — investing in Israeli real estate, or European real estate, or in some Latin American markets — often has worse fundamentals than US single-family rentals. For me, OOS investing wasn’t a preference. It was the only viable path. And the same Cleveland mistake I made would have been more expensive if I’d made it later, with more capital, after I’d told everyone I knew I was a real estate investor.

Frequently Asked Questions

Is out-of-state real estate investing profitable?

It can be, and for many investors it is. Out-of-state markets often have better price-to-rent ratios than expensive coastal cities, which makes the cash flow math work where it doesn’t locally. But “profitable” depends entirely on the market, the team, and your operating discipline. About 60% of my OOS deals have been profitable; the rest broke even or lost money. The portfolio is profitable because the winners outsize the losers, not because every deal worked.

How much money do I need to start out-of-state investing?

Realistically, $40k–$60k for a first conventional deal in a $130k–$175k market — that’s down payment (20–25% on an investment property), closing costs, initial reserves (3–6 months of mortgage + expenses), and a buffer for early surprises. Foreign nationals using DSCR loans should plan on 25–30% down plus the same reserves. If you’re doing BRRRR, you also need rehab capital up front before the refinance, so the cash requirement temporarily doubles before it comes back out.

What is the best state for out-of-state real estate investing?

There’s no single answer — the right state for you depends on your strategy, your tolerance for landlord-friendly versus tenant-friendly law, your target cash flow, and what teams you can build. The Carolinas (NC, SC), Texas, Florida, Tennessee, and Indiana are commonly cited because they combine landlord-friendly law, growing populations, and cash-flow-friendly price points. North Carolina has been my anchor market because I built a team there first and have stayed disciplined about staying in markets I know. The “best state” matters less than the depth of your team in whatever state you pick.

How do I find a good property manager out of state?

Interview at least three. Ask each one the same operational questions: how do you screen tenants, how do you handle maintenance under $500 versus over $500, what’s your average vacancy time, can I see your monthly statement template, what software do you use. Then call two of their current owner-clients (not the references they offer — find owners independently from public records or BiggerPockets). The PMs who are confident enough to give you direct owner contacts unprompted tend to be the ones worth hiring. Bad PMs are the most common cause of OOS investments going sideways, and the only way to evaluate them is to talk to people who’ve worked with them.

Can I invest out of state if I have no real estate experience?

You can, but it’s the harder path. The investors I’ve seen succeed at this without prior local experience tend to have either (a) a partner who has done it before and is personally invested in their success, (b) significant capital reserves to absorb mistakes, or (c) the discipline to do one deal and sit with it for a year before doing another. Without one of those, the learning curve is steep enough that a lot of people quit after the first painful year. If you’re considering a first-ever real estate deal as an OOS purchase, weight the option of doing one local deal first — even if the numbers are worse, the operational education is worth it.

Is out-of-state investing better than turnkey?

Different trade-offs. Turnkey is OOS investing with most of the work done for you in exchange for a markup on the property price and ongoing PM fees. You get speed and simplicity; you give up forced equity (the rehab gain that BRRRR captures) and the upside of finding off-market deals. For investors who genuinely want passive returns and don’t want to learn the operational side, turnkey is the more honest fit. For investors who want to build wealth through forced appreciation and creative deals, full OOS active investing produces more equity over time. I do active OOS — but I won’t pretend turnkey is wrong for everyone.

So is out-of-state real estate investing worth it? For me, after 24 deals and four states, the answer is yes — under the conditions in the table above. Without those conditions, the answer is no, and the cost of being wrong is real.

The honest framing for anyone deciding right now: don’t ask whether OOS investing is worth it in general. Ask whether it’s worth it for you, in the specific market you’d target, with the team you can realistically build, on the strategy that fits your capital and time horizon. The general answer is unhelpful. The specific answer is the only one that matters.

If you want a sequenced playbook for getting from where you are to your first OOS deal — the order to do things in, the parts that catch most people off guard, the things I’d have done differently in Cleveland — I put together the Remote Investor First Deal Roadmap. It’s the 7-step sequence I’d hand to someone starting today, built from what’s actually worked across 24 deals (and what hasn’t). No course pitch. No upsell. Just the order that matters.

Find out exactly where you stand before your first deal.

10 questions. A personalized score across 5 dimensions. Free.

Get my readiness score →