Key Takeaways

- FIRPTA forces the buyer to withhold 15% of the gross sale price — not 15% of your gain — and send it to the IRS within 20 days of closing

- The 15% is a deposit, not your tax bill: actual tax on a typical long-held rental is usually 5–10% of sale price

- Filing Form 8288-B before closing can reduce the withholding to match your real tax owed — the IRS takes ~90 days to issue the certificate

- On a $175k sale with ~$35k gain, the default path traps $26,250 at the IRS for 12–18 months; the 8288-B path keeps roughly $21,000 in your account at closing

- A US LLC owned by a foreign person is “disregarded” for tax purposes — FIRPTA still applies, the LLC alone doesn’t fix it

- The single most expensive mistake: discovering FIRPTA at the closing table instead of planning for it the day you go under contract

IN THIS ARTICLE

- What FIRPTA Actually Is (In Plain Terms)

- Who Counts as a “Foreign Person” Under FIRPTA

- The 15% Withholding, Walked Through on a Real $175k Sale

- How Form 8288-B Actually Works (And Why Timing Is Everything)

- What Most Foreign Investors Get Wrong About FIRPTA

- How FIRPTA Fits Into the Bigger Foreign Investor Playbook

- Frequently Asked Questions

The first time I sold a US property as a foreign national, the title company emailed me the closing statement and there it was: a line item for $26,250 wired directly to the IRS. The sale was $175,000. The 15% withholding was non-negotiable. Nobody — not the agent, not the buyer’s attorney, not the closing officer — was going to lift a finger to reduce it for me.

That’s the moment most foreign investors learn what FIRPTA is. After it’s already cost them.

Here’s what almost no one writes: the 15% withholding is not your tax bill. It’s a deposit the IRS holds against a tax bill that’s almost always smaller. And there’s a form you can file before closing that brings the withholding down to roughly what you actually owe — keeping the rest of that money in your bank account instead of in an IRS holding pattern for the next 12–18 months.

I’ll explain the mechanism, the math from a real $175k sale, and the three things foreign investors get wrong about FIRPTA — including the one that costs the most.

This is not legal advice. Talk to a US CPA who has actually filed Form 8288-B before. Past that caveat, here’s what’s actually happening.

What FIRPTA Actually Is (In Plain Terms)

FIRPTA stands for the Foreign Investment in Real Property Tax Act. Congress passed it in 1980 because foreign investors were buying US real estate, selling it for a profit, and disappearing back to their home countries before the IRS could collect a dime in capital gains tax. FIRPTA’s solution was simple: make the buyer responsible for withholding a chunk of the sale proceeds and sending it directly to the IRS.

That chunk is 15% of the gross sale price — not 15% of the profit. This is the part most foreign investors miss. The withholding has nothing to do with whether the deal made money. Sell a property for $175,000 and the buyer is required by law to withhold $26,250 and forward it to the IRS within 20 days of closing, regardless of whether you made $50,000 or lost $5,000 on the deal.

The withholding is filed by the buyer using Form 8288 and a corresponding Form 8288-A copy goes to you (the seller). Your $26,250 sits with the IRS as a deposit against your eventual tax bill. When you file a US tax return for that year (Form 1040-NR for an individual, or 1120-F for a foreign corporation), the IRS reconciles the withholding against your actual tax owed and refunds the difference.

The lag between “money taken at closing” and “refund check arrives” is typically 12 to 18 months. That’s the part that hurts.

The full IRS guidance lives on the FIRPTA withholding page — but it’s written in tax-code language, not investor language. The mechanics matter more than the citations.

Who Counts as a “Foreign Person” Under FIRPTA

This is narrower than people assume. FIRPTA applies to:

- Nonresident alien individuals — meaning you, if you’re not a US citizen or green card holder, and you don’t meet the substantial presence test (which is complicated, but if you live in Israel year-round and visit the US a couple of times a year, you’re not a US resident for tax purposes)

- Foreign corporations that haven’t elected to be treated as US corporations

- Foreign partnerships, trusts, and estates

Here’s the part that catches people: a single-member LLC owned by a foreign person is treated as a “disregarded entity” for FIRPTA purposes. This means even if you bought your rental in a US-formed LLC, the IRS looks straight through to you — the foreign owner — and FIRPTA still applies on the sale. Forming a US LLC does not by itself make you not-foreign for tax purposes.

The fix that does work — electing to have your LLC taxed as a US corporation — has its own consequences (corporate tax rates, branch profits tax, more complicated returns). It’s a legitimate strategy in some cases, not in others. This is where the CPA conversation matters. The point for now: don’t assume your LLC structure exempts you. The proper LLC setup for a foreign national real estate investor is about liability and operations, not avoiding FIRPTA.

The exemptions that do skip FIRPTA entirely are narrow: the buyer is purchasing as a primary residence and the price is $300,000 or less. That’s not your investor exit. Assume FIRPTA applies.

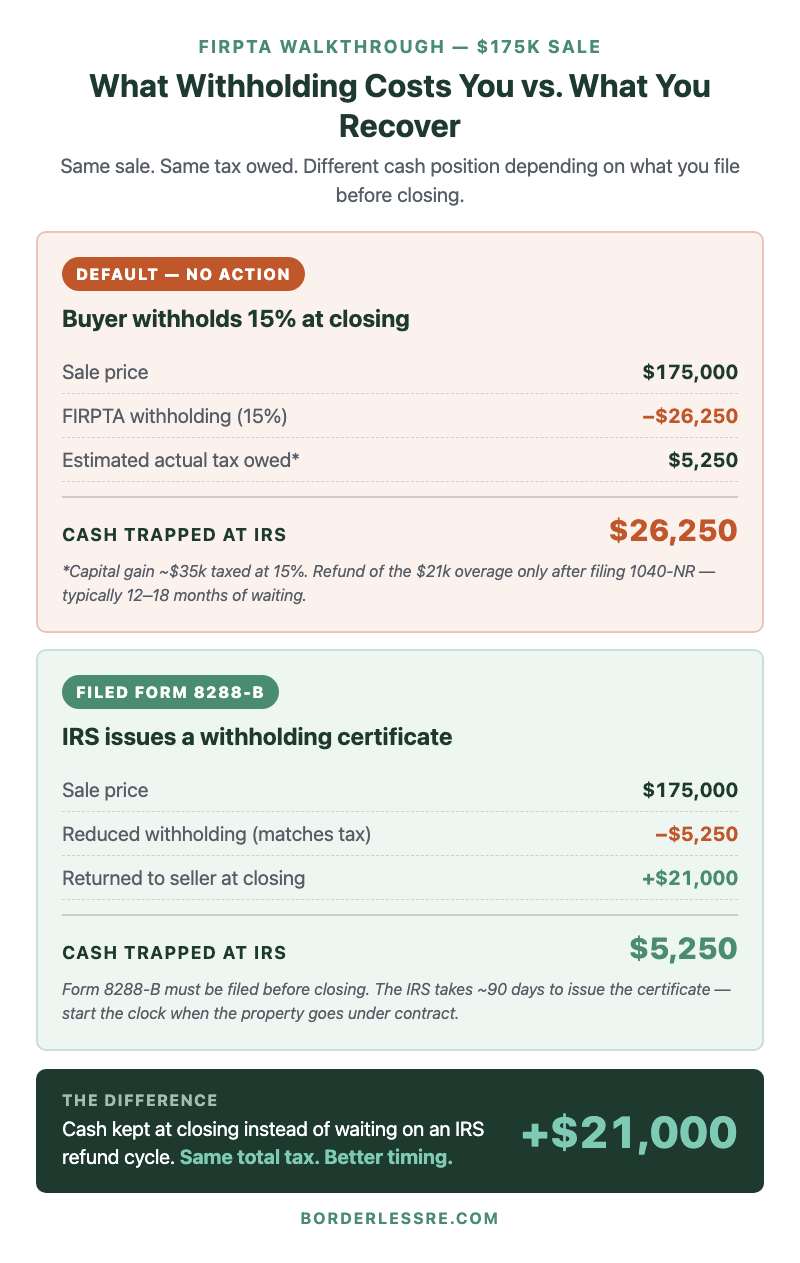

The 15% Withholding, Walked Through on a Real $175k Sale

Here’s a deal close to the real numbers from a property I exited in Kings Mountain, NC. Sale price: $175,000. I’d held it for several years, my cost basis after depreciation was around $140,000, putting my long-term capital gain at roughly $35,000. At the 15% federal long-term capital gains rate, my actual federal tax bill on the gain was about $5,250.

If I do nothing — if I just walk into closing and let the default FIRPTA process run — here’s what happens:

- Buyer withholds 15% × $175,000 = $26,250 and wires it to the IRS within 20 days of closing

- I get $148,750 in net sale proceeds (minus closing costs)

- I file Form 1040-NR the following year showing my actual tax owed: $5,250

- The IRS refunds me the $21,000 overage — typically 12 to 18 months later

That $21,000 is my money. The IRS is just holding it. But it’s frozen there for over a year, doing nothing, while the next deal I want to put it into closes without me.

There’s a different path. Before closing, I (or my CPA) can file Form 8288-B — Application for Withholding Certificate. The application says, in effect: “Here’s the proof of the actual tax I’ll owe on this sale. Please reduce the withholding to match.” If the IRS agrees, they issue a withholding certificate that overrides the default 15%, and the buyer withholds only what’s actually owed.

For my $175k sale, that means $5,250 to the IRS at closing — not $26,250. The remaining $21,000 stays in my account, ready to redeploy.

How Form 8288-B Actually Works (And Why Timing Is Everything)

The reduced withholding certificate is not a deduction or a loophole. It’s a paperwork process that pre-calculates your real tax liability and gets the IRS to agree to a smaller withholding number before the closing happens. Here’s the sequence:

- Property goes under contract. Closing is typically 30–60 days out.

- Your CPA prepares Form 8288-B, including the calculation of your projected gain (sale price minus your cost basis minus selling costs minus depreciation recapture, with applicable rates applied), and submits it to the IRS along with supporting documents.

- The IRS reviews the application. Per the IRS Form 8288-B page, processing takes approximately 90 days.

- The IRS issues the withholding certificate — or denies it, in which case the default 15% applies.

- At closing, the title company holds the FIRPTA withholding in escrow until the certificate arrives. Once received, the reduced amount is sent to the IRS and the rest is released to you.

The timing problem is obvious: 90 days of IRS processing versus 30–60 days from contract to close. If you don’t start the application early — ideally the moment the property goes under contract, not the week before closing — the certificate won’t arrive in time. The title company will withhold the full 15%, send it to the IRS, and you’ll be back to waiting 12–18 months for a refund.

This is the single most expensive timing mistake in foreign investor exits. Not because the tax changes — it doesn’t — but because cash you could be redeploying into the next deal is locked up doing nothing for over a year. On a small portfolio, $21,000 is the down payment on a $130k BRRRR property. Trapped capital is real opportunity cost.

The right move: the day your property goes under contract, email your CPA and tell them to start the 8288-B application that week. The 90-day clock starts when the IRS receives the application, not when you decide to file it.

What Most Foreign Investors Get Wrong About FIRPTA

Three things, in order of how much they cost.

Mistake #1: Treating the 15% as the tax bill. The number of foreign investors who walk away from a sale thinking they owed $26,250 in taxes — when they actually owed $5,250 and could have requested the rest back — is genuinely high. The withholding is a deposit. Your actual tax is calculated on your gain (sale price minus adjusted cost basis minus depreciation recapture), not on gross proceeds. If you don’t file a 1040-NR for that year, you forfeit the refund. The IRS will not chase you to give your money back.

Mistake #2: Discovering FIRPTA at the closing table. This is the most common version of the story. You’re under contract, a week from closing, and the title company sends over the closing statement with the FIRPTA line item. By then it’s too late to file 8288-B in time. This is why the entire exit strategy needs to be planned from the moment you decide to sell — not when the buyer’s earnest money clears.

Mistake #3: Assuming an LLC fixes it. As covered above: a single-member LLC owned by a foreign person is a disregarded entity for tax purposes, and FIRPTA still applies. The LLC is essential for other reasons — liability protection, professional credibility, banking — but it doesn’t make you not-foreign in the eyes of the IRS. Plan for FIRPTA regardless of how you took title.

The investors who handle FIRPTA well aren’t the ones with clever structures. They’re the ones who plan the exit on the same calendar as the sale negotiation.

How FIRPTA Fits Into the Bigger Foreign Investor Playbook

FIRPTA only matters at exit. If you’re at the start of your journey — no property yet, just researching — this is the tax you want to know about before you buy, so it doesn’t surprise you on the way out. The full operational picture for getting started lives in how to invest in US real estate from abroad.

The flip side: if your strategy is BRRRR and you plan to refinance and hold long-term, FIRPTA may never apply to you in any given year. You only trigger the withholding on a sale — refinancing pulls cash out without selling. This is one quiet reason the BRRRR-and-hold strategy is so well-suited to foreign investors: you can build a US portfolio with DSCR loans for non-US citizens and never realize a taxable gain until you decide to liquidate.

When you do exit, the 8288-B path is almost always worth filing if you have any meaningful cost basis. The exception: if your tax liability genuinely is close to 15% of the sale price (think a quick flip with most of the proceeds being taxable gain), the certificate doesn’t save you much. But for a long-held rental with depreciation taken and a moderate gain, the gap between 15% withholding and your actual tax owed is usually large enough to make the application a clear win.

Frequently Asked Questions

Does FIRPTA apply if I sell at a loss?

Yes. FIRPTA withholding is calculated on gross sale price, not on gain. Sell a property for $175,000 at a $10,000 loss and the buyer still has to withhold $26,250 unless you’ve obtained a reduced withholding certificate. You’d then file your 1040-NR to claim the full refund — but you wait 12–18 months for it. Filing 8288-B in advance is the only way to avoid the cash trap when you sell at a loss.

Who actually sends the withholding to the IRS — me or the buyer?

The buyer is legally responsible for the withholding. In practice, the title company or closing attorney handles the mechanics: they hold the FIRPTA amount from the seller’s proceeds at closing, file Form 8288 with the IRS, and remit the funds within 20 days. You as the seller never touch the withheld amount. You just receive net proceeds with FIRPTA already deducted.

Can the buyer face penalties if they don’t withhold?

Yes — and this is why the buyer’s title company is rigorous about it. If the buyer fails to withhold and the IRS later determines the seller was foreign, the buyer becomes liable for the unpaid tax plus penalties and interest. This is why no closing officer will quietly skip FIRPTA on a foreign seller’s exit, and why disputing the withholding at the closing table is a non-starter. The system has the buyer’s interest aligned with the IRS, not yours.

What’s the difference between FIRPTA withholding and my actual US tax owed?

FIRPTA is a withholding mechanism — a deposit. Your actual tax is the federal long-term capital gains tax on your realized gain (sale price minus adjusted cost basis minus selling costs), plus depreciation recapture (taxed at up to 25%). These calculations rarely produce a tax bill equal to 15% of gross sale price. The difference between what was withheld and what you actually owe gets refunded after you file your 1040-NR — but only if you file. Many foreign sellers don’t, and the IRS keeps the overage.

Do US tax treaties affect FIRPTA?

Generally, no — FIRPTA withholding applies regardless of tax treaty between the US and your home country. Treaties may affect how the gain is ultimately taxed (or whether you can credit the US tax against your home country’s tax), but the withholding mechanism itself is rarely overridden by treaty. This is one of the few areas where treaties don’t provide much relief. Confirm the specifics with a CPA who handles your specific country’s treaty.

Is the withholding refundable if my LLC is taxed as a US corporation?

If you’ve made the election to have your LLC taxed as a US corporation (Form 8832), then the entity is no longer a foreign person for FIRPTA purposes — and the withholding doesn’t apply at all on the sale. This is one of the clean structural fixes, but it comes with the trade-off of US corporate taxation on the entity’s income going forward. Worth modeling out with a CPA before you decide whether to elect.

FIRPTA is one of those rules that feels punishing the first time you encounter it and routine after that. The mechanism isn’t complicated. The math isn’t even complicated. What’s complicated is the timing — and the fact that no one in the closing process has any incentive to flag the 8288-B option for you.

Plan the exit on the same calendar as the sale. File 8288-B the week the property goes under contract. Don’t let $20k of your own money sit at the IRS for a year and a half because of paperwork you didn’t know existed.

If you’re earlier in the journey — still figuring out where you stand on capital, financing, market selection, and team — the Remote Investor Readiness Score breaks your situation down across five dimensions and tells you the specific gap to close before deal one. Built from 24 deals across 4 US states, done from Israel.

Find out exactly where you stand before your first deal.

10 questions. A personalized score across 5 dimensions. Free.

Get my readiness score →