Key Takeaways

- Set up the LLC before the first deal — entity-first prevents friction with title, banking, and the eventual DSCR refinance

- Form the LLC in the state where you’ll hold the property — that gives you automatic court standing for evictions, vendor disputes, and any other state-court action; Wyoming-default is the wrong starting structure for a single-property LLC

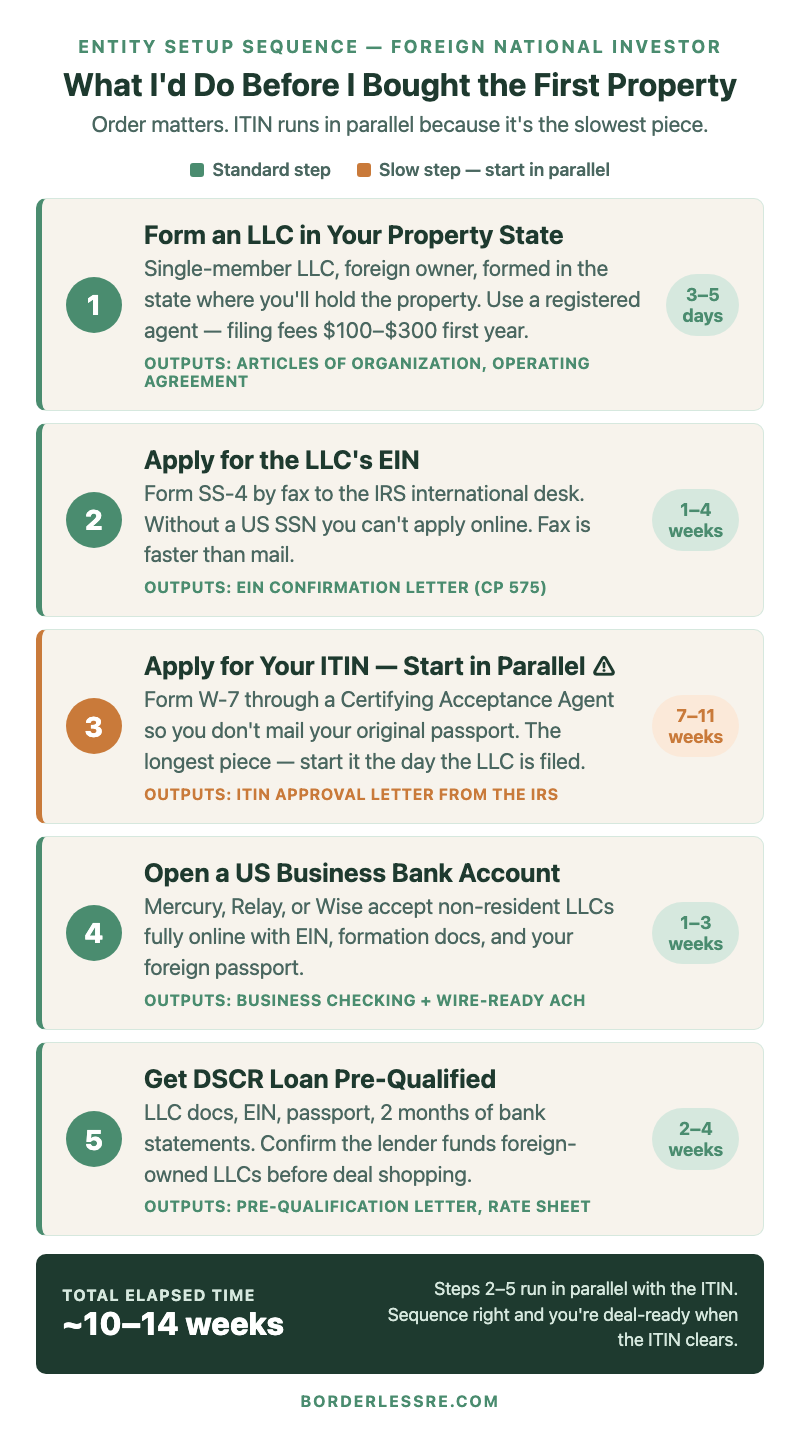

- The full sequence: LLC (3–5 days) → EIN (1–4 weeks) → ITIN (7–11 weeks, started in parallel) → US business bank account (1–3 weeks) → DSCR pre-qualification (2–4 weeks)

- Total elapsed time is ~10–14 weeks because the slow piece (ITIN) runs in parallel with everything else

- Form 5472 is the silent killer — foreign-owned single-member LLCs must file it annually or face $25,000/year penalties; almost no “how to” article mentions this

- Do all of this before deal one. My first deal closed in my personal name and the friction it created — bank holds, title questions, messy taxes — was the lesson that produced this checklist

IN THIS ARTICLE

- Why Entity-First Matters (And What Happens When You Skip It)

- Step 1: Form an LLC in Your Property State

- Step 2: Apply for the LLC’s EIN

- Step 3: Apply for Your ITIN (in Parallel)

- Step 4: Open a US Business Bank Account

- Step 5: Get DSCR Loan Pre-Qualification

- What Most People Get Wrong About Foreign-Owned LLCs

- FAQ

A quick disclaimer up front: I’m not a CPA and this isn’t legal advice. Talk to a US CPA who works with foreign investors before you file anything. What follows is the sequence I used to set up Vandelay Real Estate LLC from Israel, in the order I’d do it again — and the order I wish I’d done it the first time.

The first deal I ever closed in the US was a 2020 flip in Fayetteville, NC — bought in my personal name because I was in a hurry and didn’t have an entity in place. It worked out — $65k purchase, $35k rehab, $150k sale, $50k profit — but the process was harder than it needed to be. Title company asked questions I didn’t have clean answers to. The bank that held the wire flagged me twice. My CPA bill that year was higher than it had to be because the purchase, the rehab spend, and the sale all flowed through my personal taxes. The entity-first sequence in this post is what I wish I’d had on day one.

If you’re investing in US real estate as a foreigner and trying to figure out the legal and operational setup, this is the practitioner walkthrough — not a law firm overview. Six steps, in order, with the timelines I actually saw.

Why Entity-First Matters (And What Happens When You Skip It)

The temptation when you’re new is to find a deal first and “figure out the structure later.” This is exactly backwards. The structure determines what’s possible at every subsequent step.

Here’s what skipping the entity step actually costs you. Without an LLC, the property has to close in your personal name — which means your foreign passport on the deed, your foreign address on county records, and your name in front of the title insurance underwriter. Some title companies will close anyway. Others will pause for compliance review and add 5–10 days to your timeline. None of them love it.

Without an LLC, you also can’t open a US business bank account before closing — meaning your down payment wires originate from a foreign personal account, which triggers FinCEN-style scrutiny at most US banks. My first wire from Israel in 2020 got held for 4 days while the bank verified the source of funds. The seller almost killed the contract.

Without an LLC, your refinance options shrink dramatically. Most DSCR lenders — the financing vehicle that makes investing in US real estate as a foreigner workable in the first place — require the property to be vested in an LLC at refinance. So even if you bought in your personal name, you’d have to quitclaim into an LLC later, which can trigger the due-on-sale clause on your acquisition loan and create a fresh title insurance issue.

The LLC isn’t a tax optimization. It’s the foundation that the next four steps stand on. Set it up first.

Step 1: Form the LLC in the State Where You’ll Hold the Property (3–5 Business Days, $100–$300 First Year)

Form the LLC in the state where the property will be located. Not Wyoming, not Delaware, not Nevada — the state you’re actually buying in.

The reason most “form a Wyoming LLC” articles skip: court standing. If a tenant stops paying and you have to file an eviction, you file it in the property’s state court. A Wyoming LLC trying to evict a tenant in a Texas property has to first register as a “foreign LLC doing business in Texas” with the Texas Secretary of State before it has the legal capacity to file in Texas court. Without that registration, the court can dismiss your eviction, and you’ve burned weeks while the tenant stays rent-free. The same standing issue applies to vendor disputes, contractor mechanics’ liens, insurance claims, and any other action your LLC will ever take or defend in the property’s state. Forming directly in the property state makes standing automatic.

The Wyoming/Delaware/Nevada pitch you’ll see online (privacy, low fees, asset protection) is real for holding companies and operating businesses with no fixed location. It’s not the right structure for a single-property real estate LLC whose entire reason for existing is to own one asset in one specific state.

The mechanics: hire a registered agent in your target state ($100–$200/year). They file the Articles of Organization with the state’s Secretary of State on your behalf, draft a basic Operating Agreement, and provide a registered office address. Filing fees vary by state — North Carolina is $125, South Carolina is $110, Florida is $125, Georgia is $100, Tennessee is $300, Texas is $300. Most landlord-friendly Sun Belt states run $100–$300 first year and $50–$200/year after.

What you’ll have at the end: an EIN-ready LLC with two documents — Articles of Organization (the state-issued formation certificate) and the Operating Agreement (the internal governance document). Save digital copies. You’ll send these to every lender, bank, and title company for the rest of the LLC’s life.

Once you’re past 5–10 properties spread across multiple states, a holding-company structure (a parent LLC in Wyoming or Delaware owning child LLCs in each property state) starts to make sense for asset protection and consolidated bookkeeping. That’s a portfolio-scale decision driven by the cost of running multiple state-specific entities — not the right starting structure for property #1.

Step 2: Apply for the LLC’s EIN (1–4 Weeks)

The EIN (Employer Identification Number) is the tax ID for your LLC. You need it before you can open a bank account or sign a lender application.

If you have a US Social Security Number, you can apply online and get the EIN immediately. As a foreign national without an SSN, you have two options:

Fax the SS-4 form to the IRS international desk (recommended). On line 7b of Form SS-4, write “Foreign” instead of an SSN/ITIN. Fax the form to the IRS international fax number listed on the IRS Form SS-4 instructions page. Turnaround is typically 1–2 weeks. The IRS faxes the EIN confirmation back to the number you put on the form.

Mail the SS-4 to the IRS. Same form, same line 7b, just slower. 4–6 weeks.

I used the fax route through my CPA. Got the EIN back in 9 days. Some registered agent services will handle the SS-4 filing for you for an extra $100–$200 — worth it if you want to avoid setting up an international fax line.

Watch out for one thing: there are dozens of “EIN service” websites that charge $300–$500 to file the SS-4 on your behalf. The IRS does not charge anything for an EIN. The form is free. Pay your CPA or your registered agent if you want help with the form, but don’t pay a marketing site that’s just refiling a free IRS form.

You’ll know it’s done when you receive the CP 575 notice from the IRS — that’s your official EIN confirmation. Save the digital copy. Banks and lenders will ask for it.

Step 3: Apply for Your ITIN (Start in Parallel — 7–11 Weeks)

This is the slowest piece, which is exactly why most people get it wrong. They wait until they’ve found a deal and a lender to start the ITIN process — and then they’re stuck waiting two months while the deal goes cold.

Start the ITIN application the same week your LLC is formed. It runs in parallel with everything else.

The ITIN (Individual Taxpayer Identification Number) is your personal US tax ID as a foreign national. You need it to file US tax returns on rental income, to claim treaty benefits, and to satisfy lenders who want a tax ID for the LLC’s owner on file.

The process: file IRS Form W-7 with a certified copy of your passport. The mistake foreigners make is sending their original passport to the IRS — which means going without a passport for 2–3 months. Don’t do this.

Use a Certifying Acceptance Agent (CAA) instead. CAAs are authorized by the IRS to verify your identity documents without mailing the originals. Many CAAs work with foreign clients via video call — you show your passport on camera, they certify it, you keep the physical document. I used a CAA in New York for my ITIN. The whole verification took 30 minutes over Zoom.

CAA fees range from $300–$500. Worth every dollar to keep your passport.

Once filed, the IRS takes 7 weeks during normal periods and 9–11 weeks if you file during tax season (January 15 to April 30). You’ll receive a CP 565 notice in the mail when it’s approved.

If you start this on day one of LLC formation, by the time you’ve completed steps 4 and 5 (banking and DSCR pre-qualification), the ITIN is either approved or close to it. Your timeline collapses by the same weeks the ITIN takes — you don’t add the wait, you parallelize it.

Step 4: Open a US Business Bank Account (1–3 Weeks)

A foreign-owned LLC can’t walk into a Chase branch and open an account anymore. Most US brick-and-mortar banks now require at least one signer with a US Social Security Number for business accounts. The workaround used to be flying to the US to open the account in person, which was a $2,000 trip for a banking transaction.

That changed when fintech business banks and multi-currency accounts started accepting non-resident LLCs. Three options that work today, all of them online-only and remote-friendly:

Mercury (mercury.com) — accepts non-resident LLCs with EIN, formation documents, and the foreign owner’s passport. Online application takes 30 minutes. Approval in 3–7 business days for clean applications. No monthly fees, free wires, multiple sub-accounts. This is what most foreign investors I know use as the LLC’s primary US business checking account.

Relay (relayfi.com) — similar profile to Mercury, also non-resident-friendly, slightly stronger sub-account/team-access features if you have a property manager who needs view-only access.

Wise Business (wise.com) — multi-currency account with US dollar account details (routing + account number) plus 40+ other currencies. Where Wise earns its place in this stack: cheap, fast international transfers from your home currency to USD before the money ever touches the LLC’s US bank. A foreign-bank-to-Mercury wire typically costs $30–$50 and takes 2–3 days; the same transfer through Wise generally clears same day at near-mid-market FX rates. Most foreign investors I know run Mercury (or Relay) as the LLC’s primary checking and Wise as the FX bridge for funding the LLC from outside the US.

What you’ll need to upload during the application: Articles of Organization, EIN confirmation letter (CP 575), Operating Agreement, your passport, and a US address for the LLC (your registered agent’s address works). Some banks ask for a basic business description — write something like “Real estate investment holding company; rental property ownership in [state]” and you’re fine.

Once the account is live, the LLC owns its own US-based wire and ACH rails. Down payment wires originate from the LLC. Rent deposits go into the LLC. Refinance proceeds land in the LLC. The personal account stays out of the property workflow entirely — which is exactly what you want for clean books and a clean tax filing.

Step 5: Get DSCR Loan Pre-Qualification (2–4 Weeks)

The financing piece is where most of the foreign national content stops being practical. The truth: pre-qualification is the gate. Until a lender has put a rate sheet in front of you, you don’t actually know what you can offer on a property.

A DSCR (Debt Service Coverage Ratio) loan is the financing instrument that doesn’t require US W-2 income or a US credit history. It qualifies on the property’s cash flow — rent ÷ PITI ≥ 1.0. There’s a longer breakdown in the DSCR loan guide for non-US citizens.

To get pre-qualified before you have a property, you’ll need:

- LLC formation documents (Articles, Operating Agreement)

- EIN confirmation letter

- Passport (the lender will copy the photo page)

- 2 months of bank statements (LLC account if open, otherwise personal foreign account)

- Source-of-funds letter from your foreign bank if the down payment is coming from outside the US

- Confirmation the lender funds foreign-owned LLCs (ask explicitly — some lenders quote you and then decline at underwriting once they see a non-US owner)

A pre-qualification letter gives you: the maximum LTV the lender will offer, a rate range based on current pricing, and a confirmation that you’re a real borrower. It’s what your real estate agent will show listing agents to prove you can close.

Most lenders will pre-qualify you in 2–4 weeks if your documents are clean. Then you have 60–90 days to use the pre-qualification before they’ll re-pull. Time it so the pre-qual is fresh when you start making offers.

If you’ve done steps 1–4 and started the ITIN in parallel, by the time the ITIN clears (week 10–11), you have an LLC, an EIN, a US bank account, and a DSCR pre-qualification. Total elapsed time: about 10–14 weeks. You’re now in a position to underwrite deals seriously and close fast when the right one comes up.

What Most People Get Wrong About Foreign-Owned LLCs

Two specific traps that almost every “how to set up an LLC as a foreign national” article skips. Both will cost you real money if you don’t know about them.

Trap 1: The Form 5472 reporting requirement. A foreign-owned single-member LLC is treated as a “disregarded entity” for US tax purposes — meaning the LLC itself doesn’t file a tax return. Most foreigners hear “no tax return” and stop reading. The trap: a foreign-owned disregarded LLC is still required to file Form 5472 + a pro-forma Form 1120 every year, reporting any “reportable transaction” with the foreign owner (which includes contributing capital to the LLC, taking distributions, lending money to the LLC — almost everything you’ll do). The penalty for not filing is $25,000 per year per missed form, raised from $10,000 in 2018. The IRS published full guidance on the Form 5472 reporting rules. I have seen foreign investors find out about this rule three years into their portfolio. The retroactive penalty exposure is brutal. Get a CPA who specifically knows foreign-owned LLC compliance — not just any CPA — before the first tax filing deadline after you form the LLC.

Trap 2: The series LLC vs. multiple LLCs decision. As your portfolio grows, you’ll start thinking about asset protection — should each property be in its own LLC? Should you use a series LLC structure? The seminar circuit will sell you on a 12-LLC setup with a Wyoming holding company before you’ve closed your second deal. For most investors with under 10 properties in a single state, this is overkill and expensive. Each LLC costs ~$150–$300/year to maintain (registered agent, annual report, separate tax filings). My structure for the first 8 deals: a single LLC formed in NC where most of my properties were, holding everything in that state directly. Once I had 10+ properties spreading across NC, SC, and TN, I formed separate state-specific LLCs in each property state and started looking at a Wyoming or Delaware parent to consolidate filings. The structure followed the portfolio — not the other way around. Don’t pay for protection (or complexity) you don’t yet need.

FAQ

Do I need to be in the US to set up an LLC?

No. Every step in this post can be done from outside the US. The LLC formation is filed by a registered agent in your property state. The EIN is issued by fax to the IRS. The bank account is opened online with Mercury, Relay, or Wise. The ITIN is verified by a Certifying Acceptance Agent over video call. The DSCR pre-qualification is fully remote. I set up Vandelay Real Estate LLC from my desk in Tel Aviv. I have never set foot in any of my LLC’s filing states.

How much does it cost to set up a US LLC as a foreign national?

Total first-year setup: roughly $750–$1,500 depending on which services you use and which state you file in. State filing fee ($100–$300 depending on the state), registered agent (~$150), CAA fee for ITIN (~$400), CPA consultation (~$200–$500). Recurring annual cost after year one is about $200–$400 (registered agent + state annual report + ongoing CPA fees that scale with the portfolio).

Should I form a Wyoming or Delaware LLC for the privacy and asset-protection benefits?

For a single-property real estate LLC, no. The friction outweighs the benefits: you’ll have to register the Wyoming LLC as a “foreign LLC doing business” in the state where the property sits anyway (which means paying both states’ fees), and you give up automatic court standing for evictions and vendor disputes in your property state. Wyoming and Delaware become useful as a parent-company layer once you already have multiple state-specific LLCs to consolidate under one roof — typically past 5–10 properties spread across multiple states.

What if I want to use a single LLC to buy properties in multiple states?

You can, but you’ll need to register the LLC as a “foreign LLC doing business in [State]” in every additional state where you hold property. Each registration costs $100–$300 plus the ongoing annual filing in each state. Past 2–3 states, the math usually pushes investors toward separate state-specific LLCs (with consolidated bookkeeping) instead of one LLC registered everywhere. A CPA familiar with multi-state real estate structures can run the cost comparison for your specific portfolio.

What if I already bought a property in my personal name — can I move it into an LLC later?

Yes, via a quitclaim deed transferring title from you to the LLC. Two issues to watch: (1) it can trigger a “due-on-sale” clause on your acquisition loan (most lenders won’t enforce, but it’s a risk), and (2) it requires a fresh title insurance update. Talk to your title company before you do it. The cleaner path is to set up the LLC first — which is the entire point of this post.

Do I need a separate LLC for each property?

Not at first. One LLC holding multiple properties in the same state is fine for a small portfolio. As the portfolio grows past ~10 properties, or as individual property values climb above ~$300k, splitting into separate LLCs (or using a holding-company structure) starts making sense for asset protection. Build the structure your portfolio actually needs — not the structure a course is selling you.

The setup is the foundation. The deal flow, the team building, the market selection, the financing — all of that comes after the entity is in place. If you want the full overview of how to invest in US real estate from abroad, that’s the pillar post. If you’re earlier in the process and want to know what a non-US citizen actually needs to buy investment property in the USA, start there.

If you want to see where you actually stand on the entity-and-financing readiness piece — what’s done, what’s missing, and where the gap is for your specific situation — that’s exactly what the Remote Investor Readiness Score is built to surface. The Legal & Entity Setup dimension scores this directly.

Find out exactly where you stand before your first deal.

10 questions. A personalized score across 5 dimensions. Free.

Get my readiness score →