Key Takeaways

- BRRRR out of state is the same five letters — Buy, Rehab, Rent, Refinance, Repeat — but the operational mechanics are different from a local BRRRR. You’re trading proximity for system, and the system has to be airtight from underwriting through refinance.

- The 2022 Kings Mountain NC deal is the cleanest example I have: $100k purchase + $30k rehab → $175k appraisal → 100% OPM (zero of my own money in) → $500/month cash flow. Done from Israel, never visited.

- The phase that breaks remote BRRRRs most often isn’t the rehab. It’s the refi appraisal. If your ARV comes in low, the whole capital recycling math breaks. Most of the work that protects against this happens before you make the offer.

- The financing question (how a foreign national gets the loan) is a separate problem covered in BRRRR for foreign nationals. This post is the operational playbook — what you do once the financing is figured out.

- The system below works whether you’re a US investor running the cycle 1,500 miles from home or an international investor running it 7,000 miles from home. The mechanics are identical.

IN THIS ARTICLE

- How to Do BRRRR Out of State Without Watching the Property

- Phase 1: Underwrite — Where Most Remote BRRRRs Are Won or Lost

- Phase 2: Acquire — Closing Without Setting Foot Inside the Property

- Phase 3: Rehab — The Phase Most Likely to Break Without On-Site Eyes

- Phase 4: Refinance — Where the Capital Comes Back Out (or Doesn’t)

- Phase 5: Rent — Cash Flow Starts Here, Not at Refi

- What Most People Get Wrong About BRRRR Out of State

- Frequently Asked Questions

How to Do BRRRR Out of State Without Watching the Property

The honest version of how to do BRRRR out of state is this: the strategy is the same one David Greene wrote a book about in 2017, but the operating discipline is different. Local BRRRR investors can drive by during rehab, walk the property before the appraisal, eyeball whether the contractor actually did the work. Remote BRRRR investors can’t do any of those things. Every step of the cycle has to produce verifiable outputs that you can review without being there. If a step doesn’t produce verifiable outputs, you have a problem you’ll discover at the worst possible time — at the refi appraisal, when you find out the rehab was thinner than the photos suggested.

I’ve done ten BRRRRs from Israel since 2021. Six worked the way the strategy is supposed to work — equity forced through rehab, refinance pulls most or all of my capital back out, property cash flows on the back end. Two had refi appraisals come in lower than expected and trapped capital in the deal that I wasn’t planning to leave there. Five Cleveland properties never reached the refinance step in any meaningful way and got exited as the wrong properties in the wrong market. The pattern across the wins and losses is the same: the deals that worked had structure at every phase before the phase began. The deals that didn’t were trying to figure out the structure as they went.

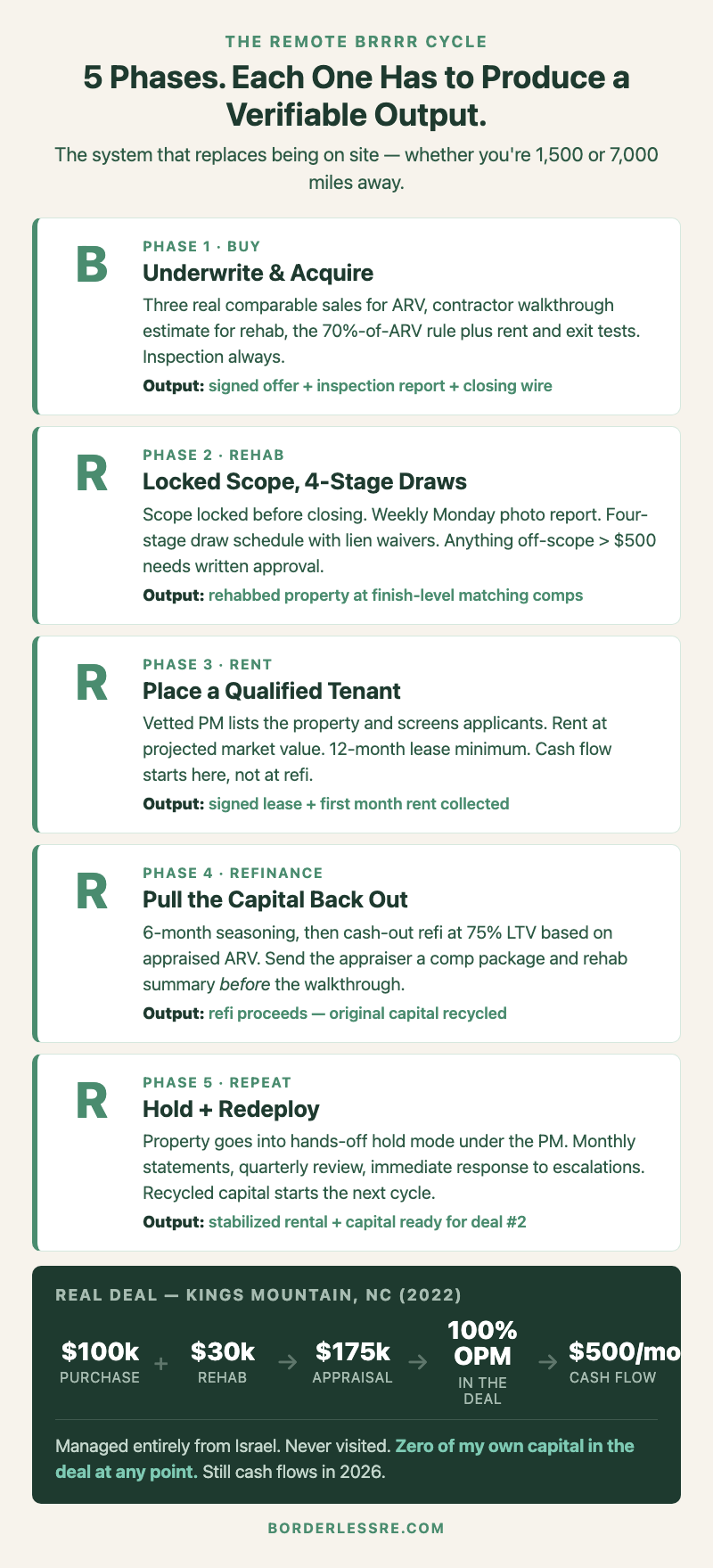

This post is the structure. Five phases — Underwrite, Acquire, Rehab, Refinance, Rent — each with the specific outputs you need before you move to the next phase. The 2022 Kings Mountain deal is the worked example because it ran cleanly through all five phases at full distance: 100% other people’s money in, 100% remote operation, and a $500/month cash-flowing rental on the other side. If you’re new to out-of-state real estate investing generally, read that first; this is the BRRRR-specific operational manual on top of the general remote investing framework in the long distance real estate investing pillar.

Phase 1: Underwrite — Where Most Remote BRRRRs Are Won or Lost

The single most important phase is also the one most beginners shortchange. Underwriting is not the spreadsheet. Underwriting is the validation that the spreadsheet’s assumptions match reality. The reason this matters more remotely is that you can’t fix bad underwriting at the closing table by walking the property — every assumption has to be verified through documents, photos, and third-party inspections before money changes hands.

The numbers I run on every BRRRR before submitting an offer:

ARV (after-repair value) — the most consequential number in the entire deal. This is what the appraiser will assign to the property after the rehab is done, and it’s the number the refinance is based on. The right way to determine ARV is not Zillow. The right way is three comparable sales pulled by the agent in the last 6 months, within a half-mile radius, with similar bed/bath count and square footage, that have been renovated to roughly the standard you’re going to renovate to. If the agent can’t pull three real comparables, the market doesn’t have enough data to BRRRR safely. Walk away.

Rehab budget — built from a contractor’s walkthrough estimate, not from a per-square-foot rule of thumb. The contractor goes through the property in person (you watch the video), itemizes scope by trade, prices materials and labor, and gives you a number with a 10–15% contingency on top. If the contractor estimates a number without a walkthrough, the number isn’t real. Demand the walkthrough.

The 70% rule, refined. Standard BRRRR underwriting says: purchase + rehab ≤ 70% of ARV. That’s the right starting point but it’s not enough on its own. I run two additional checks: the rent test — does the projected monthly rent cover PITI plus a 30% buffer for vacancy/maintenance/capex? If not, the cash flow won’t survive a normal year. The exit test — if I had to sell this property in 12 months instead of refinancing, could I get my money out? This forces you to underwrite for the bad scenario where the refi falls through.

Holding costs — every month between purchase and refinance is real cost: hard money interest (typically 11–13% annualized), insurance, property taxes, utilities. Plan for 4–6 months of holding on a remote BRRRR, sometimes longer. Bake those costs into the deal at underwriting, not at the end.

Where the Kings Mountain deal underwrote: $100k purchase, $30k rehab, $175k projected ARV. That’s $130k all-in into a $175k value, or 74% of ARV — slightly above the 70% threshold but defensible because the seller financing structure (more on that in Phase 2) eliminated the holding cost on the purchase side, which made the deal economics work even at the higher ratio. The rent projection was $1,200/month, which after PITI of $700 and the 30% buffer left $360/month of expected cash flow. Final cash flow turned out to be $500/month because the rent came in higher than projected and the property tax was lower. Not by accident — by underwriting for conservative numbers and letting reality come in better.

The single biggest underwriting failure mode for remote investors is using ARV numbers from the listing agent (who wants the deal to close) without independent verification from your buyer’s agent. The listing agent’s ARV number is sales material, not analysis. Get your own.

Phase 2: Acquire — Closing Without Setting Foot Inside the Property

The acquisition phase has three discrete pieces: the offer, the inspection, and the closing. Each has remote-specific mechanics.

The offer. I make offers from a desk in Tel Aviv on properties I’ve never seen. The mechanics: my agent runs comparable sales analysis, sends me the property listing, walks the property on video, and sends me the rehab estimate from my contractor. I review all of it, send the offer terms in writing, and the agent submits. The whole sequence takes 2–4 days from listing to offer. The discipline that makes this work is having an agent and a contractor whose judgment you trust through track record, not a single conversation. If you’re buying in a new market, you need to build that track record on the team before the first offer — see how to find a property manager out of state for the team-vetting process; the same logic applies to agents and contractors.

The inspection. Non-negotiable. I hire a home inspector for $400–600 to do a full inspection and send me the written report with photos. I read the report myself, not just the summary the agent sends. The inspection is where you find the things the listing agent didn’t disclose: foundation cracks, roof age, HVAC end-of-life, electrical or plumbing issues. If the inspection turns up something material that wasn’t in the rehab estimate, I either renegotiate the price down by the cost of that work or walk away. Walking away has happened — the inspection is the cheapest insurance against an underwriting error.

The closing. Closings in 2026 are routinely done by mail/DocuSign for remote investors. The title company sends documents to your notary (mine is a US-based service my attorney coordinates), you sign and notarize, courier them back, and wire the funds the day before closing. I’ve never been to a closing in person. The mechanics are mature enough that a remote closing is, if anything, faster than an in-person one.

The Kings Mountain deal acquired through a structure that’s worth highlighting because it eliminated the down payment problem entirely. The seller financed the purchase: $100k purchase price, seller carried back the note at favorable terms, no traditional bank involved at the buy stage. My contractor financed the $30k rehab through his line of credit and was paid back at the refi. My total out-of-pocket through the entire acquisition phase: around $5k of inspection, transaction, and earnest money costs. The 100% OPM structure isn’t always available, but when it is, it’s transformative for the remote BRRRR investor — your capital is uncommitted until the refi, which means you can move on multiple deals in parallel and pick the best one at refinance time.

Phase 3: Rehab — The Phase Most Likely to Break Without On-Site Eyes

The rehab is the longest phase (typically 8–16 weeks) and the one where the most can go wrong without active management. The system that protects against rehab failure is the system in how to flip houses remotely — locked scope of work before closing, weekly Monday photo reports, four-stage draw schedule with lien waivers, change-order rule for anything above $500. Every BRRRR rehab gets the same treatment.

The BRRRR-specific wrinkle is that the rehab has to optimize for two things at once: the property has to rent at the projected rent, AND it has to appraise at the projected ARV. Those are usually aligned but sometimes pull in different directions. A finish-out that wins a tenant (LVP flooring, fresh paint, new appliances, basic landscaping) costs less than a finish-out that wins an appraiser (granite counters, tiled bathrooms, refinished hardwoods, premium fixtures). For a rental, you want the cheaper finish-out and a higher cash-flow margin. For the refinance appraisal, you want the more expensive finish-out and a higher ARV.

The way I split the difference on most BRRRRs is to invest in the structural and mechanical scope (roof, HVAC, electrical, plumbing) at full quality, do mid-grade interior finishes (LVP not hardwood, painted cabinets not new ones, clean tile not premium tile), and skip the truly premium upgrades that wouldn’t change the appraisal much in the price band the property is in. Below $200k ARV, premium finishes don’t proportionally lift the appraisal — appraisers are looking at comparable sales at similar finish levels, and if the comparables are mid-grade, premium upgrades don’t move the number. Above $300k ARV, the calculus shifts and premium finishes start to pencil. Match the finish-out to the price tier of the comparables.

On Kings Mountain, the rehab budget was $30k for a property bought at $100k targeting $175k ARV. That’s roughly $20/sqft on a 1,500 sqft house — modest but adequate for the price band. Scope: new roof, HVAC tune-up, electrical panel update, plumbing rough-in fixes, full interior paint, LVP through the main floor, refinished cabinets, mid-grade fixtures, basic landscaping. Came in at $31k actual against $30k budgeted — close enough that the change-order rule barely fired. Took 11 weeks from closing to ready-to-list.

The single most expensive rehab mistake remote investors make is over-improving for the price band. A $200/sqft rehab finish on a $150/sqft market property doesn’t appraise at $200/sqft — it appraises at the market price band. The extra $50/sqft just becomes trapped capital. If you can’t tell the difference, ask your agent and your contractor to confirm the finish level matches the comparable sales used in the ARV. They’ll know.

Phase 4: Refinance — Where the Capital Comes Back Out (or Doesn’t)

The refinance is where the BRRRR cycle either delivers on its promise or doesn’t. The mechanics are: 6-month seasoning period after closing on the rehab loan, then apply for a 30-year cash-out refinance based on the property’s appraised value, typically at 75% loan-to-value. The proceeds pay off the rehab loan and any remaining purchase loan, and whatever is left over comes back to you as recycled capital.

Two things usually go wrong at this phase, and both have remote-specific dimensions.

Problem 1: The appraisal comes in below ARV. This is the failure mode that turns a winning BRRRR into a trapped-capital BRRRR. If your projected ARV was $175k and the appraisal comes in at $155k, your 75% LTV refi is $116k instead of $131k — that’s $15k of capital that stays in the deal indefinitely, plus the cash flow math gets worse because the refi loan is smaller and the cost basis is higher than planned. The way to prevent this is the conservative ARV underwriting in Phase 1, plus the rehab finish-level matching in Phase 3. If you’ve done both well, the appraisal usually comes in close to projection. If they were sloppy, the appraisal is where you find out.

The remote-specific dimension: I can’t be at the appraisal in person. I can prepare for it. What I send the appraiser through my agent — before the appraisal walk-through — is a list of comparable sales (the same three I used in Phase 1, or better ones that have closed since), a copy of the rehab scope and final budget, and a list of improvements that may not be obvious from a quick walkthrough (HVAC age, roof age, foundation work, electrical updates). Appraisers typically receive this information well; it gives them ammunition to support the higher value, and many appraisers are working with limited time on each property and appreciate having the data organized.

Problem 2: The financing falls through or the rate has moved. The seasoning period between closing and refi is usually 6 months. Rates can move significantly in 6 months. The refi assumption you underwrote with may not be available when you actually go to refinance. The way to manage this is to pre-qualify with your refi lender at closing — get a rate hold or a conditional commitment if possible, even if it’s only good for 60–90 days. Then re-engage the lender 30 days before the seasoning period ends to lock the rate. For foreign nationals, the refi mechanics are a separate problem set covered in DSCR loans for non-US citizens — DSCR loans are the standard refi vehicle, qualifying based on the property’s rental income rather than personal income.

On Kings Mountain, the refinance came in clean: appraisal at $175k matching projection, 75% LTV refi at $131k, paid off the seller-financed purchase note ($100k) and the rehab note ($30k), with about $1k of net proceeds left over. Most importantly, the structure pulled all of my $0 of original capital out of the deal — there was nothing to pull because nothing went in — and the property went into hold mode cash-flowing $500/month from a 100% leveraged position. That’s the math BRRRR is built for.

Phase 5: Rent — Cash Flow Starts Here, Not at Refi

The rent phase is operationally the longest of the five (it’s the rest of the property’s life), but operationally simplest. The hard work was done in Phases 1–4. By the time you reach Phase 5, you have a rehabbed property with a refinanced loan, a property manager in place from the team-building phase, and a tenant who was placed during or just before the refi. The rest is steady-state operation.

The key Phase 5 decisions are tenant placement and lease structure. Tenant placement is the PM’s job, and the PM vetting process you ran before buying is what makes this phase work. Lease structure is mostly standard — 12-month initial lease with option to renew at market, deposit equal to one month’s rent, pet policy, late-fee schedule. Long-term holding usually means 1–2 year lease cycles with periodic rent increases at renewal.

The thing remote investors get wrong about Phase 5 is over-engagement. Once the property is rehabbed, refinanced, and rented to a qualified tenant managed by a vetted PM, the right amount of investor involvement is monthly review of the PM’s statement, quarterly portfolio review, and immediate response to anything escalated by the PM. Beyond that, hands off. If you’re checking in weekly on a stabilized rental, the PM doesn’t need to be there — and a stable PM you’re micromanaging will eventually quit.

The exception is if the property is part of a foreign-investor portfolio with FIRPTA implications on exit — see FIRPTA explained for foreign real estate investors for the planning side of that. Not all holds need to factor exit tax into the operating decisions, but international investors should be tracking exit timing and reduced-withholding-certificate eligibility from year one of the hold, not figuring it out three months before sale.

Kings Mountain has been in Phase 5 since 2022. The tenant has renewed twice, the rent has been raised once, the cash flow has been steady at $500/month with periodic capex events (HVAC service, water heater replacement) that the reserve covers. The PM sends a monthly statement, I review it once a month, and the property runs without further intervention. That’s what BRRRR Phase 5 should look like. The operational work in the first four phases is what buys you a hands-off Phase 5.

What Most People Get Wrong About BRRRR Out of State

The conventional wisdom on remote BRRRR comes from local BRRRR practitioners who are extending advice across geography without changing the system. That’s the source of most of the failure modes.

Mistake 1: Treating BRRRR as a way to get rich quick from a distance. It isn’t. BRRRR is a way to compound equity over years through forced appreciation and capital recycling. The compounding is real and the math is unusually good for remote investors compared to traditional buy-and-hold, but the timeline on a single deal is 6–12 months from acquisition to refinance, plus an indefinite hold. Investors expecting a faster cycle are usually disappointed and quit before the system has time to compound. Treat your first BRRRR as a 12-month learning project, not a transaction. The second one is faster because you’ve built the team. The fifth one is much faster.

Mistake 2: Underweighting the refi. Most beginner BRRRR content focuses on the buy and the rehab. The refi is the most consequential phase because it’s where the capital recycling actually happens. A BRRRR that closes the buy and the rehab but never refinances is not a BRRRR — it’s a buy-and-hold with extra steps. Underwrite the refinance assumptions as carefully as you underwrite the purchase. Rate environment, seasoning period, lender qualification criteria, appraisal logistics — all need to be modeled before the offer. The refi is not a phase you can improvise.

Mistake 3: Building the strategy before building the team. The remote BRRRR system depends on three high-trust relationships: agent, contractor, and PM. None of those can be built in two weeks. Investors who try to compress the team-building phase and dive into BRRRR with new relationships almost always have at least one phase break — usually the rehab — because the trust hasn’t been established to support the operational decisions that have to be made under uncertainty. Build the team for 3–6 months in any new market before you BRRRR. The investors I’ve seen succeed at remote BRRRR all spent more time on the team than they did on the first deal.

Mistake 4: Trying to BRRRR in a market that doesn’t support it. Not every market has the price-to-ARV ratio to make BRRRR work. High-cost coastal markets usually don’t — there isn’t enough margin between purchase price and ARV to refinance the capital out at 75% LTV. Distressed Rust Belt markets sometimes don’t — the appraisals don’t come in at the projected ARV because the comparable sales aren’t there. The right BRRRR markets are usually mid-tier, price-to-rent friendly, with active rehab activity that supports comparable sales at improved values. North Carolina, Indiana, Tennessee, and parts of the Carolinas and Texas all qualify in 2026. New York, San Francisco, and most of California don’t, on the BRRRR math. Pick the market for the strategy, not the strategy for the market.

The international-investor specific failure mode worth flagging: assuming the timeline in your home country applies to the US BRRRR cycle. The US closing process is 30–45 days; the rehab is 8–16 weeks; the seasoning period for refinancing is 6 months; the refinance closing is another 30–45 days. Total time from acquisition offer to capital recycled: typically 9–12 months. International investors who model this as a 4–6 month cycle (the way local BRRRRs sometimes run) end up over-leveraged on cash flow during the seasoning period. Plan for the longer timeline.

Frequently Asked Questions

What is the BRRRR method in real estate?

BRRRR stands for Buy, Rehab, Rent, Refinance, Repeat. It’s a strategy for building a rental portfolio by acquiring distressed properties below market value, renovating them to force equity appreciation, renting them to qualified tenants, refinancing based on the new appraised value to recycle most or all of the original capital, and repeating the process with the recycled capital. Done correctly, the strategy compounds equity faster than traditional buy-and-hold because each deal extracts capital that funds the next one.

Can you do BRRRR remotely from another state?

Yes. About half of all BRRRR investors operating in 2026 are doing at least one out-of-state deal, and a growing minority (myself included) are operating across multiple states from a single home base. The mechanics are identical to local BRRRR — Buy, Rehab, Rent, Refinance, Repeat — but the operational discipline is different. Every phase has to produce verifiable outputs (photos, inspection reports, draw schedules, appraisal data) that you can review without being on site. Investors who try to remote-BRRRR with a “I’ll figure it out as I go” mindset usually have a phase break in the rehab or the refinance.

How long does a BRRRR cycle take?

Plan for 9–12 months from acquisition offer to refinance closing on a typical remote BRRRR. Breakdown: 30–45 days from offer to acquisition closing, 8–16 weeks for rehab, 6 months of seasoning before the refi (this is mandated by most refi lenders), and 30–45 days for the refi closing. Local BRRRRs can sometimes compress this to 6–8 months because the rehab phase moves faster with active on-site management. International investors should plan for the full 12 months.

How much money do I need to start a BRRRR out of state?

Realistically, $40k–$70k for a first traditional BRRRR in a $130k–$180k market — that’s down payment on a hard-money or DSCR purchase loan, full rehab budget out of pocket, holding costs through the seasoning period, and a reserve for surprises. Creative-finance structures (seller financing, 100% OPM) can reduce this to under $10k as in the Kings Mountain example, but those structures require existing relationships and aren’t where beginners should start. Plan for the higher number on your first deal.

Is BRRRR still profitable in 2026?

Yes, in the right markets. The BRRRR math depends on the spread between purchase-plus-rehab cost and after-repair value, plus the rent-to-PITI relationship at refi. Markets where this math works in 2026: North Carolina (Fayetteville, Winston-Salem, Newton, Hickory), Indiana, parts of Tennessee, parts of the Carolinas, parts of Texas. Markets where it doesn’t: most coastal cities, most premium suburbs. Higher rate environment in 2024–2026 has compressed the math compared to 2020–2022, but the strategy still works in markets that combine reasonable acquisition prices, strong rent-to-price ratios, and active comparable sales.

What’s the biggest risk in remote BRRRR?

The refinance appraisal coming in below the projected ARV. This is the scenario that turns a winning BRRRR into a trapped-capital BRRRR — your refi loan is smaller than planned, less of your original capital comes out, and the cash flow math gets worse. The way to manage this risk is by being conservative on the ARV at the underwriting stage, matching the rehab finish level to the comparable sales the appraiser will reference, and proactively providing the appraiser with a comp package and rehab summary before the walkthrough. Investors who do all three rarely have appraisal surprises.

What’s the difference between BRRRR for foreign nationals and BRRRR out of state?

Different problems. The financing question (how a non-citizen qualifies for the loan and the refi) is covered in BRRRR for foreign nationals — DSCR financing, ITIN setup, LLC structuring. The operational question (how to run the cycle without visiting the property) is covered in this post and applies equally to a US investor and an international investor once the financing is in place. A US investor running a BRRRR in another state and an international investor running a BRRRR in the US both face the same operational challenge: replacing presence with system.

So how do you do BRRRR out of state? The same way you do BRRRR locally — but with every phase enforced through verifiable outputs instead of in-person checks. Underwrite conservatively. Acquire with inspection and remote closing. Rehab through scope, draws, and lien waivers. Refinance with appraisal preparation. Rent through a vetted PM. The Kings Mountain deal — $100k + $30k → $175k → 100% OPM → $500/month — is what the math looks like when all five phases run cleanly. Most of mine have, after I learned the system. Some haven’t, when I tried to skip a phase.

This is the last post in the first three months of the BorderlessRE content plan, and it’s intentionally the densest one — because by now there are eleven other posts that explain individual pieces of the system. The REACH framework pillar is the spine. The PM vetting process is the team-building piece. The DSCR loan post is the financing piece. The remote rehab system is the rehab piece. This post is what happens when you put all of those together on a single deal. If you’ve read the cluster, you’ve already got the components. This is the assembly instructions.

The Remote Investor Readiness Score is the next step if you’re trying to figure out where in the system you actually are. Ten questions, five dimensions, and a personalized identification of the gap that’s keeping you from your first BRRRR. No course pitch. Just the score and the next post in the cluster you should read.

Find out exactly where you stand before your first deal.

10 questions. A personalized score across 5 dimensions. Free.

Get my readiness score →