Key Takeaways

- Long distance real estate investing works when the system is built before the deal — pick the market, build the team, then buy. Reverse that order and you become a case study other people learn from.

- The REACH framework (Research, Engage, Acquire, Control, Harvest) is the same five steps whether you live in California buying in Indianapolis, or in Tel Aviv buying in North Carolina. The work is identical. The setup cost is different.

- Most pillar guides on this topic were written for the US-domestic out-of-state investor. This one extends the framework to the international/foreign-national case: DSCR financing, ITIN setup, international wires, and FIRPTA on exit.

- I’ve done 24 deals across 4 US states from Israel since 2020. Five of them (Cleveland, 2021) were the wrong properties in the wrong market with the wrong team — I exited that cluster between 2023 and 2026. The other 19 are why I’m still doing this.

- The biggest mistake at every level — beginner to scaling — is treating market selection as the most important decision. It isn’t. Team selection is. A good team in a B-market beats a great market with a bad team every single time.

IN THIS ARTICLE

- What Long Distance Real Estate Investing Actually Means in 2026

- The REACH Framework: Five Steps That Work the Same Whether You’re 500 or 7,000 Miles Away

- Step 1: Research — Pick the Market Before You Pick the Property

- Step 2: Engage — Build the Team Before You Need It

- Step 3: Acquire — Buy at 65–70% of ARV (and Finance It Right)

- Step 4: Control — Manage the Asset, Not the Property

- Step 5: Harvest — Convert Equity to Cash Flow at the Right Stage

- What Most People Get Wrong About Long Distance Real Estate Investing

- The International-Investor Layer: What Changes When You’re Doing This From Outside the US

- Frequently Asked Questions

- Where to Go From Here

What Long Distance Real Estate Investing Actually Means in 2026

Long distance real estate investing is buying and operating rental property in a market you don’t live in and can’t drive to in an afternoon. That’s the whole definition. The investor in San Francisco buying in Cleveland is doing it. So is the investor in Tel Aviv buying in Fayetteville. The friction is the same in kind — different in degree.

I’ve done 24 deals across North Carolina, Ohio, South Carolina, and Texas since 2020. I’ve never lived in any of them. Most of the properties I own I have never physically visited. The portfolio is now around $4M in active assets and projects with roughly $2,300 a month in active rental cash flow on top of about $1.9M in projected sale value across active builds. That isn’t a flex — it’s the proof that the system in this guide works at scale.

The thing that has changed since David Greene published Long-Distance Real Estate Investing in 2018 is the second audience. In 2018 the canonical book on this topic was written for the US-domestic investor moving capital to a different US state. In 2026 there is a second audience — the international investor with capital outside the US — and almost no independent practitioner content speaks to them. The financing infrastructure caught up (DSCR loans for foreign nationals are real and they work), but the operating playbook didn’t. This guide is both. The framework is universal. The international layer is the section that earns the unique angle.

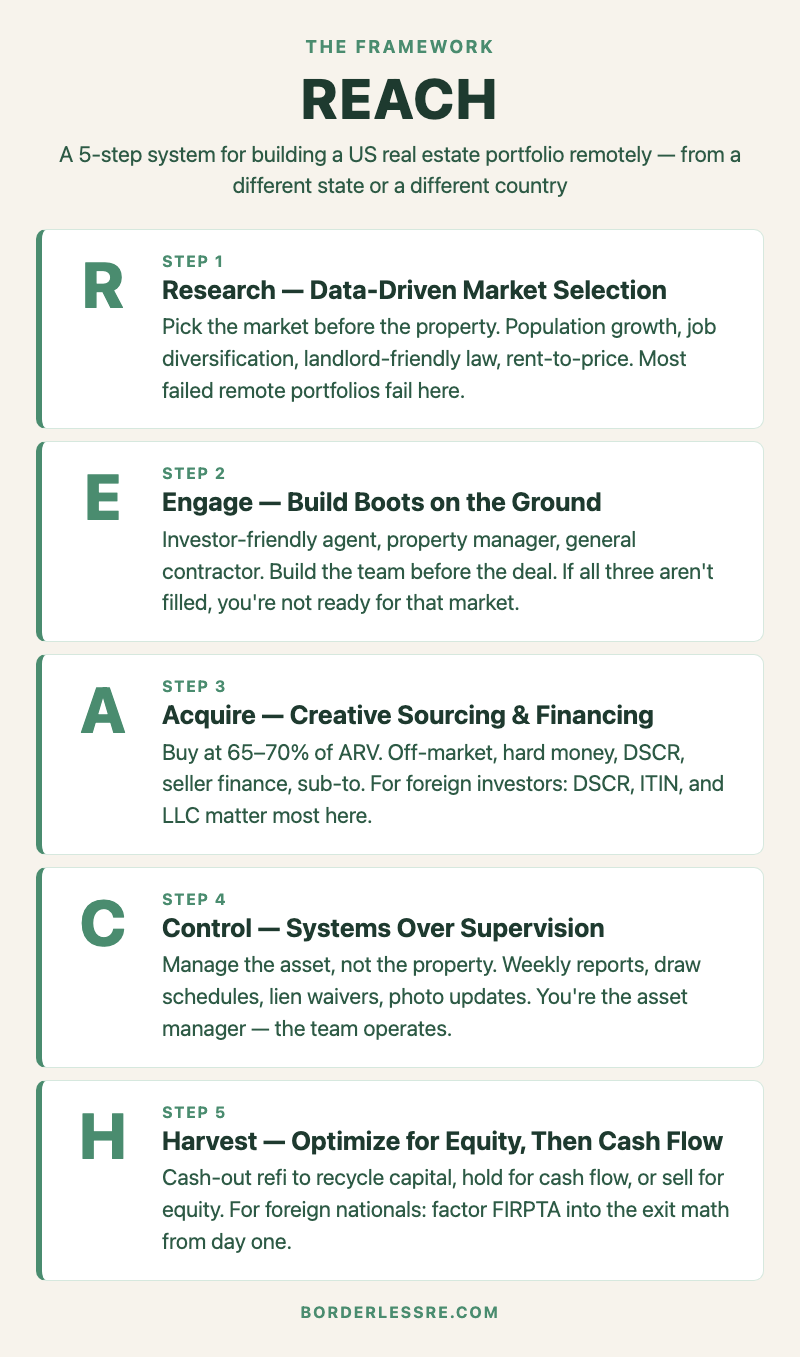

The REACH Framework: Five Steps That Work the Same Whether You’re 500 or 7,000 Miles Away

I built REACH because I needed a checklist that I could run on a market and a deal whether I was sitting in Tel Aviv at 11pm or on a phone call with a builder at 7am. The five steps are Research, Engage, Acquire, Control, Harvest. Every deal I’ve done that worked moved through those five in that order. Every deal that didn’t work either skipped one or did them out of sequence.

The reason the framework matters more than any single tactic inside it is that remote investing fails at the seams between steps, not inside them. People who fail at long distance real estate investing usually didn’t fail at finding a property — they failed at building a team that could close it, or at building a control system that could manage it once they had it. REACH makes the seams visible.

A note before the breakdown: this is a pillar guide, which means it’s the map. Each step has its own deeper post in the cluster — financing, FIRPTA, BRRRR mechanics — and I’ll link to them where they go deeper than this post can. Treat this as the spine. The detail posts are the ribs.

Step 1: Research — Pick the Market Before You Pick the Property

Most beginner remote investors pick a property first and then justify the market it’s in. That’s backwards. The market is the bigger decision. A mediocre property in a strong market still appreciates and stays rented. A great property in a weak market becomes a multi-year capital drag. I learned that the expensive way in Cleveland.

In 2021 I bought five single-family BRRRRs in Cleveland — three solo, two with a partner. The deals looked good on paper. Purchase prices between $80k and $93k, rehabs between $20k and $24k, projected appraisals at $116k to $146k, projected cash flow around $300 to $350 per door. The “perfect BRRRR” of the cluster (deal #6) hit $88k purchase, only $6k rehab, $146k appraisal. The math worked. The market didn’t. Tenants cycled, maintenance ate the cash flow, and exit liquidity was thinner than I’d modeled. I exited all five between 2023 and 2026 — some at small losses, some at break-even, the partnership deals at modest profit only because we held them long enough for the market to catch up.

The cost of being wrong about a market is rarely catastrophic. It’s a few years of capital tied up in a place that wasn’t compounding. That’s why market research is the first step — you can’t undo it later without a sale.

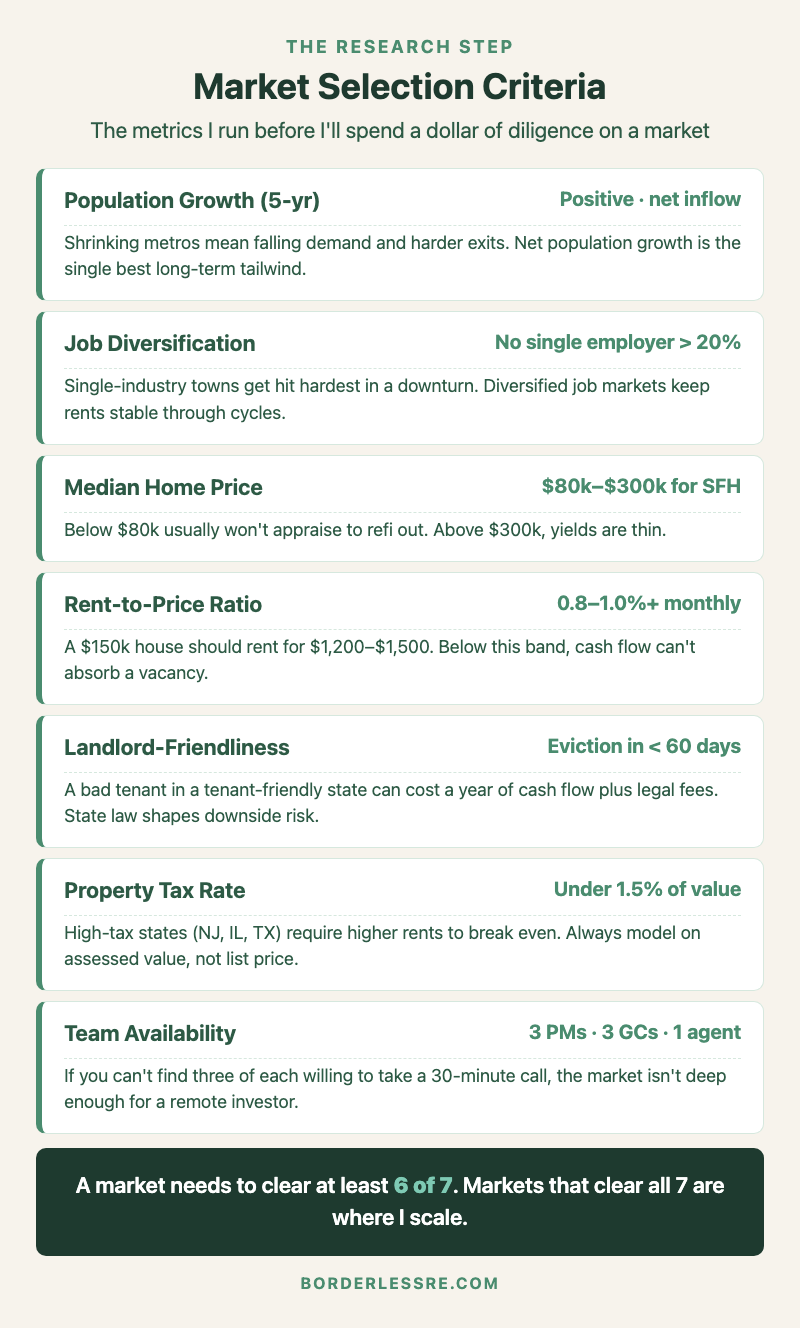

Here’s the screen I run before I’ll spend a dollar of diligence on a market:

The non-obvious one on that list is the last row — team availability. If you can’t find three property managers, three general contractors, and one investor-friendly agent willing to take a 30-minute call before you’ve bought a single property, the market isn’t deep enough for a remote investor. Cleveland, in 2021, didn’t fail my numbers screen. It would have failed the team-depth screen if I’d had one then. I do now.

For the foreign-national reader: layer one more filter on top of this. Some markets have state-level restrictions on foreign ownership now (Florida, Texas, several others have introduced rules over the last two years). If you’re buying from outside the US, confirm with a local real estate attorney before you put a market on the shortlist. The full out-of-country setup sequence is in how to invest in US real estate from abroad — read that alongside this section if international ownership is your situation.

Step 2: Engage — Build the Team Before You Need It

This is the step that decides whether you’re a remote investor or a tourist. The investor in the market is one person. The team in the market is everything else.

The five roles are: investor-friendly agent, property manager, general contractor, real estate attorney, and CPA. The first three are core operators — you’re in weekly contact with them. The last two are specialists — engaged per deal or per quarter. You need all five before you close on anything.

The hardest of the five to vet from a distance is the property manager. The PM is your operating partner — they decide which tenants get in, how fast turnovers happen, whether maintenance gets caught early or late. A bad PM can turn a $400/month cash flow into break-even by year two. The way to vet one remotely is to ask about specifics, not philosophy. What’s your screening process? What’s your average turnover time? What’s your rent collection percentage in the last 12 months? What does your monthly statement look like — can you send me a sample? If the answers are vague, the operation is vague.

The general contractor is the second hardest. The way I’ve solved this over six years is to anchor in one or two markets and work with the same builder repeatedly. The trust is earned over multiple deals — I trust my builder’s call on a deal because I’ve seen him be right hundreds of times. Trying to do a flip or a heavy rehab in a market where you haven’t built that trust yet is the most common way to lose money fast.

The agent matters because they source the deals. Investor-friendly is a real distinction — most retail agents don’t understand ARV, comps for distressed properties, or how a BRRRR investor actually models a deal. The agent who can run those numbers in their head and bring you the off-market property is rare and worth holding onto.

For the international investor: add a sixth role early — a US-based bookkeeper who can run your LLC’s books and coordinate with your CPA at year-end. The accounting overhead of a US LLC owned by a foreign person is real, and trying to handle it from a different time zone in a different language is more cost than it’s worth.

Step 3: Acquire — Buy at 65–70% of ARV (and Finance It Right)

Acquire is where remote investors lose the most money the fastest. The reason is simple: when you can’t drive by the property, you have to be more disciplined about the math, not less. The buy-side discipline is the entire margin of safety.

The number I run every deal against is 70% of after-repair value (ARV) minus rehab costs. If purchase plus rehab is more than 70% of ARV, the deal doesn’t have enough room to refinance the cash back out — which means it’s not a BRRRR, it’s a buy-and-hold with trapped capital. That’s not always wrong, but it should be a conscious choice. The deals in the portfolio that worked best all came in at 65% to 70% of ARV.

Two examples from real deals. The 2021 Fayetteville BRRRR: $102k purchase, $18k rehab, $165k appraisal. That’s $120k all-in into a $165k value — 73% of ARV. Right at the line. The cash-out refi pulled out essentially everything I’d put in, and the property still cash flows $350 a month today. The 2022 Kings Mountain BRRRR: $100k purchase, $30k rehab, $175k appraisal. That’s $130k into $175k — 74% of ARV, which I made work because the financing structure was 100% other people’s money (zero out of pocket) and the cash flow is $500 a month. Same framework, different financing.

Financing is where the international and US-domestic paths split. A US investor with W-2 income can use conventional mortgages, hard money for rehabs, and standard refinances. A foreign national can’t — the conventional underwriting requires US tax returns and US credit history. The path that works for foreign nationals is the DSCR loan, which qualifies based on the property’s projected cash flow rather than the borrower’s personal income. The full breakdown of how DSCR loans actually work for non-citizens — the lenders, the rates, the documentation, the seasoning periods — is in DSCR loans for non-US citizens.

The other thing the international investor needs to know about Acquire is the wire mechanics. When you’re closing a US property from abroad, the earnest money deposit and the closing funds wire from your bank to the title company’s escrow account. International wires take 1–3 business days, sometimes longer in compliance review, and the receiving institution has to be set up to receive them. I’ve had deals where the timing of the wire decided whether we made the closing date. Build a 5-business-day buffer into every offer if you’re wiring from abroad.

For the BRRRR strategy specifically — the one I’ve used most and the one that compounds equity fastest for remote investors — the foreign-national mechanics are unique enough that they deserve their own deep-dive. That’s the BRRRR method for foreign nationals — read it after this if BRRRR is the strategy you’re building toward.

Step 4: Control — Manage the Asset, Not the Property

Control is the step where domestic out-of-state investors and international investors finally feel the same friction. After closing, the work is the same: keep the property occupied, keep tenants happy enough to stay, catch maintenance early, and trust your team to do the day-to-day so you can do the asset-level decisions.

The mental shift here is that you are not the property manager. You are the asset manager. Your job is reviewing the monthly statement, asking the questions that catch small problems before they grow, deciding when to renew a lease vs. raise rent, deciding when to push for a turnover and when to negotiate. The PM does the operating. You do the steering.

The reporting cadence I’ve settled on after six years: weekly photo update during any active rehab (sent by the GC), monthly P&L from the PM (rent collected, expenses paid, balance forwarded), quarterly portfolio review where I look at all properties together and decide whether anything needs intervention. That’s it. If you’re checking in more than that, you’re micromanaging. Less than that, you’re not paying attention.

The thing that breaks Control is silent failure — a tenant stops paying, a maintenance issue gets ignored, a contractor goes over budget without telling you. The defense is structural, not behavioral. Lien waivers on every contractor draw. Reserve account funded to 6 months of expenses on every property. Eviction process triggered automatically at 30 days late, not negotiated case by case. These are the systems that make Control work from 7,000 miles away — they make the consequences of silent failure recoverable.

For the international investor, one more layer at this step: time zones. I’m 7 hours ahead of North Carolina, 8 ahead of South Carolina, 8 ahead of Texas, 7 ahead of Ohio. Every operational call happens in my evening or my early morning. The way I’ve made this sustainable is by batching — three calls in one block of 2 hours, twice a week, rather than scattering them through the day. The team knows my schedule. The schedule is the system.

Step 5: Harvest — Convert Equity to Cash Flow at the Right Stage

Most real estate content treats cash flow as the goal from day one. My framework is the opposite: accumulate equity first, convert to cash flow at the end. That’s a contrarian position in a niche that’s mostly built around “$5k/month passive income in 12 months” promises, and it’s the one that has actually built the portfolio.

Here’s what Harvest looks like in practice. The first BRRRR (Fayetteville 2021) — held for cash flow because the loan was already refinanced and the cash was already out, so the $350/month is pure compounding. The Cleveland cluster (2021) — Harvest meant exit. I sold all five between 2023 and 2026, recovered most of the capital, and redeployed it into new construction in North Carolina and creative-finance deals in South Carolina and Texas. The Fayetteville and Newton portfolio refinances of 2026 — equity pulled, cash redeployed into two new states (Columbia SC and San Antonio TX) for $30k and $32k of my own money into $280k assets each.

The principle is that equity is mobile. Once you’ve forced appreciation through a rehab and a refinance, that equity isn’t stuck — you can pull it, redeploy it, compound it across markets. The cash flow on any individual property matters less than what the equity is doing in aggregate.

For the international investor, Harvest is the step where FIRPTA shows up. When a foreign person sells US real property, the buyer is required to withhold 15% of the gross sales price for the IRS. That’s withheld from the closing — it doesn’t disappear, you can recover most of it through your US tax return — but it changes the cash dynamics of an exit. The reason this matters at the planning stage, not the exit stage, is that it affects how you think about hold periods and capital recycling for an international portfolio. The full FIRPTA breakdown — how the withholding works, when it doesn’t apply, how to file for a reduced withholding certificate — is in FIRPTA explained for foreign real estate investors. Read that before you exit your first US property if you’re a foreign national. It’s the post I wish I’d had before my first sale.

What Most People Get Wrong About Long Distance Real Estate Investing

The conventional wisdom on this topic is mostly bad. Three things, in order of how much they cost.

Mistake #1: Treating market selection as the most important decision. It isn’t. Team selection is. A good team in a B-market beats a great market with a bad team every single time. Cleveland is a perfectly viable market for some investors today. It wasn’t viable for me in 2021 because the team I assembled couldn’t compensate for my distance. The Reddit shorthand “out-of-state investing is dangerous” is wrong about the cause — the danger is rarely the geography. It’s the thinness of the team holding the geography together. I’ve covered the question of whether the geography itself is worth it in is out-of-state real estate investing worth it — that post is the honest yes-and-no answer with the conditions spelled out.

Mistake #2: Believing cash flow projections from a spreadsheet. Every property I’ve ever bought projected positive cash flow on the analyzer. About half of them actually delivered it in year one. Maintenance reserves get hit, vacancies happen, evictions happen, capex events happen. The realistic operating margin on a single-family rental is much thinner than most online calculators suggest. If your deal only works at the projected number, it doesn’t really work. Build in a buffer of at least 30% on operating expenses before you call a deal a winner.

Mistake #3: Treating long distance investing as a way to start. It’s a way to scale, not a way to start. The investors who do remote real estate investing as their first-ever real estate purchase have a much higher failure rate than the investors who did one local deal first to learn the operational reality. If you’ve never been a landlord, never managed a turnover, never coordinated a contractor — adding 1,500 miles of distance to your first try is harder than it needs to be. The exception is investors with no viable local market — this is most foreign investors, including me. Israel doesn’t have a real long-distance-investing-equivalent market for non-citizens with US-comparable yields and law. We get the rougher learning curve as a structural condition. If you have a viable local market and you’re choosing remote investing for “better numbers,” consider local first.

The fourth thing — the one nobody talks about — is that long distance investing is a leverage multiplier on your system. It magnifies a good system and it magnifies a bad one. The work is on the system, not the geography. Most posts on this topic frame remote investing as inherently risky. It isn’t. It’s neutrally amplifying. What you’re actually betting on is the discipline of your own process.

The International-Investor Layer: What Changes When You’re Doing This From Outside the US

Everything above applies to a US-domestic out-of-state investor and to an international investor in roughly equal measure. This section is the additional work the international investor has to do that the US-domestic investor doesn’t.

Entity setup. US LLC owned by a foreign person, with an EIN, registered in a state that’s friendly to foreign owners (Wyoming, Delaware, and the state where you’re investing are the typical choices). Operating agreement drafted with foreign ownership in mind. This is the foundation — every property goes inside the LLC, every wire flows through it, every tax filing references it.

ITIN. Individual Taxpayer Identification Number — required for the IRS to track your tax filings since you don’t have a Social Security number. The application takes 2–4 months. Start it before you start shopping for properties.

US bank account. Some banks will open accounts for foreign-owned LLCs remotely (Mercury, Relay, a few others). Others require a visit. The bank account is what receives rent from the PM, sends wires to contractors, and pays the mortgage. Without it, you’re trying to operate a US business through a foreign account, and the friction is constant.

DSCR financing. Conventional mortgages require US tax returns and credit history. DSCR loans qualify based on the property’s projected cash flow. Rates are 1–2 points higher than conventional, terms are usually 30-year fixed or 30-year with a 5/1 ARM, and most DSCR lenders for foreign nationals require 20–30% down. This is the financing path that has unlocked the post-2020 wave of international US real estate investors.

International wires. Every transaction touches an international wire. Earnest money, closing funds, refinance proceeds going home, distributions out of the LLC. The wire infrastructure is mature but not free — expect $30–$50 per wire on the sending side, sometimes a similar fee on the receiving side, and 1–3 business days clearance. Build the time and cost into every deal.

FIRPTA on exit. Already mentioned. The 15% withholding on gross sales price is the cash-flow reality of selling a US property as a foreign person.

Time zones. Already mentioned. Batch your operational calls.

The setup for an international investor takes 3–6 months before you’re ready to make a first offer. Plan for it. Most international investors who fail at US real estate fail in this setup phase — they get frustrated by the timeline, skip a step, and then run into it on the closing or the first refinance. Front-load the setup work and the rest of the investing process is the same as it is for a domestic investor.

Frequently Asked Questions

What is long distance real estate investing?

Long distance real estate investing is buying and operating rental property in a market you don’t live in and can’t drive to in an afternoon. The market can be a different state in your own country, or it can be a different country entirely. The mechanics are the same — you can’t see the property in person, so you operate through a team on the ground (agent, property manager, general contractor) and a system of remote reporting (monthly P&Ls, weekly photo updates during rehab, quarterly portfolio reviews).

Is long distance real estate investing a good idea?

Long distance real estate investing is a good idea when you have a clear market thesis, a vetted team in that market, and the operational discipline to manage from a distance. It’s a bad idea when you’re picking a market based on cash flow numbers from a spreadsheet, haven’t built a team yet, or are using it as your first-ever real estate purchase. The “is it a good idea” question depends entirely on whether the system around the investment exists.

How much money do I need to start long distance real estate investing?

For a single-family BRRRR in a $100k–$200k market, plan for $40k–$60k of starting capital — enough to cover the down payment (or all-cash purchase if using hard money), the rehab, holding costs during the rehab, and a 6-month operating reserve. Creative-finance strategies can reduce this further (I’ve done deals with $0 of my own money in), but those require existing relationships and are not where beginners should start. For an international investor, add another $5k–$10k for setup costs (LLC formation, ITIN application, US bank account, attorney and CPA setup).

Can I invest in US real estate from another country?

Yes. There are no citizenship or residency restrictions on foreign nationals owning US real estate — you have the same property ownership rights as a US citizen. The differences are operational: you’ll need a US LLC, an EIN, an ITIN, a US bank account, and a financing path that doesn’t require US credit history (DSCR loans are the standard solution). Some states have introduced restrictions on foreign ownership for specific nationalities (Florida, Texas) — confirm with a local attorney before targeting a market.

How do I find a property manager for a remote rental?

Get three referrals from the local real estate investor community (Facebook groups, BiggerPockets forums for that market, the agent who’s helping you source deals). Interview all three on the phone. Ask about their screening process, their typical turnover time, their rent collection percentage in the last 12 months, and ask for a sample monthly statement. Avoid PMs who are vague about specifics or who manage thousands of doors — for a small portfolio, a mid-size PM (200–500 doors) usually gives you better attention. Pay attention to how fast they respond to your inquiry — that’s a preview of how they’ll respond when you’re a client.

What’s the best market for long distance real estate investing?

There’s no single best market. The best market for you is the one that clears the seven-criteria screen above (population growth, job diversification, median home price in the right band, rent-to-price ratio of 0.8–1.0%+, landlord-friendly law, property tax under 1.5%, team availability) AND where you can actually build a real team. My center of gravity is North Carolina because the team is there. For another investor, it could be Indianapolis, Birmingham, Memphis, or Cleveland (yes, Cleveland — for an investor with a different team than I had in 2021). Pick the market the team makes possible, not the market the spreadsheet makes attractive.

How do I manage rehabs from another country?

Through structural systems, not personal supervision. A scope-of-work document signed before any work begins. A draw schedule (typically 25% / 25% / 25% / 25% tied to milestones). Lien waivers signed by the GC at every draw. Weekly photo updates from the GC. A budget contingency of 15–20% of the rehab cost reserved upfront. Video walkthroughs at key milestones — pre-rehab, mid-rehab, and final. The principle is the same as for a US-domestic remote investor, just with a longer time-zone gap and more reliance on the GC’s reporting discipline.

Do I need to visit the property before buying?

No, but you should be able to send someone you trust to walk it. I’ve bought properties I’ve never seen — the Fayetteville BRRRR, the Kings Mountain BRRRR, the Newton duplex, the Columbia and San Antonio creative-finance deals. The diligence is done through the agent’s walk video, an inspector’s report, and a contractor’s rehab estimate based on a walkthrough. The “you must see it in person” rule is real estate folklore, not a real requirement. What is required is that someone on your team has seen it and you trust their judgment. That’s the team-building work — once it’s done, the in-person visit is unnecessary.

What’s the biggest mistake international investors make with US real estate?

Underestimating the setup phase. Most international investors who fail at US real estate fail in the 3–6 month period before their first deal — they skip the LLC setup, delay the ITIN application, try to use a foreign bank account for a US property purchase, or get surprised by the documentation requirements of a DSCR loan at closing. Front-load the setup and the actual investing is the same as it is for a US-domestic investor. Skip steps in the setup and you’ll meet them again on the closing date.

Where to Go From Here

If you’ve read this far, the next step is figuring out where you actually stand — what’s already in place for you, and what’s missing. That’s a different question from “what do I do next” and it’s the one most investors at this stage skip.

I built the Remote Investor Readiness Score for this exact reason. It’s 10 questions about your situation — capital, market, team, financing, entity setup — and it gives you a personalized score across 5 dimensions plus a specific identification of your biggest gap. Three minutes to complete. Sent to your inbox immediately. It’s the only way I know to translate “the framework makes sense” into “here’s what I do this month.”

Take the readiness score. Then come back to whichever section of this guide your weakest dimension points to. The supporting posts in the cluster are organized to back-fill the section of REACH that you most need to build out.

The framework is universal. The path through it is yours.

Find out exactly where you stand before your first deal.

10 questions. A personalized score across 5 dimensions. Free.

Get my readiness score →