Key Takeaways

- The BRRRR method works for foreign nationals — the refinance uses a DSCR loan, not your US credit history

- DSCR loans qualify the property, not the borrower: rent ÷ PITI ≥ 1.0 is the key ratio

- Hard money covers the acquisition; DSCR cash-out refinance at 75% LTV returns your capital

- Fayetteville deal #2: $102k in, $18k rehab, $165k appraisal, $123k refi — zero dollars left in the deal, $350/month cash flow

- You need an LLC, an ITIN, and a foreign national DSCR lender — not a US credit score or W-2

- The five BRRRR steps are the same; only the financing tool at the refinance step changes

The BRRRR method is the most powerful wealth-building strategy in US real estate. Buy a distressed property, renovate it, rent it, refinance it to pull your capital back out, and repeat. Done right, you build a portfolio of cash-flowing properties with none of your original money still trapped in them.

Here’s what almost nobody writes: it works for foreign nationals too. You just need a different financing stack at the critical step — the refinance.

I’m a foreign national. I’ve done the BRRRR method 10 times across North Carolina and Ohio. My first BRRRR was deal #2, a 2021 Fayetteville, NC single-family that I purchased for $102,000, rehabbed for $18,000, and refinanced after a $165,000 appraisal — pulling all my capital out. That property still cash flows $350/month. I never visited it.

This is how the model works when you’re not a US citizen.

What BRRRR Is (The Version That Actually Matters)

Five letters. Five steps. One compounding loop.

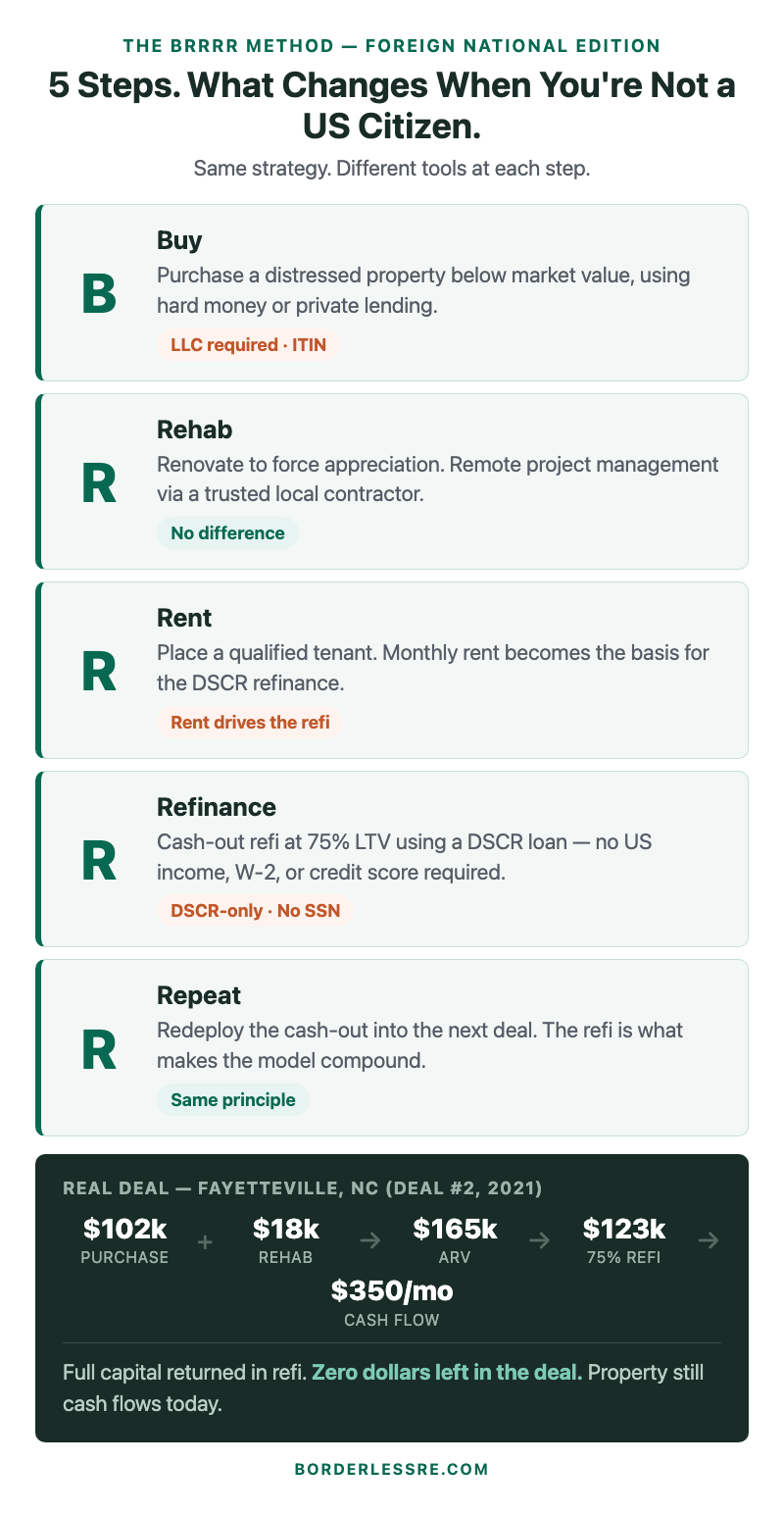

B — Buy: Acquire a distressed property below market value. The discount is where you manufacture equity. Without a discount, the rest of the strategy breaks.

R — Rehab: Renovate to force appreciation. You’re not waiting for the market to appreciate you to a higher value — you’re creating it through capital improvement. A $20,000 rehab that raises the appraisal by $50,000 is where the model gets interesting.

R — Rent: Place a qualified tenant. The rent isn’t just income — it’s the input that determines whether you can refinance. The DSCR (Debt Service Coverage Ratio) calculation compares your monthly rent to your projected mortgage payment. No tenant means no income means no refinance.

R — Refinance: Cash-out refinance at 75% of the new appraised value. This is what separates BRRRR from a standard buy-and-hold. You pull out cash — ideally more than you put in — and that cash goes into the next deal.

R — Repeat: The refinanced capital funds the next acquisition. Each time you execute a full cycle, you add a cash-flowing asset to the portfolio without permanently tying up your own capital.

The math is what makes it work. Buy at a discount, force appreciation through rehab, refinance at 75% of the higher value. If the numbers are right, you get your money back — and an asset that pays you every month indefinitely.

The Foreign National Problem — and the Solution

Traditional refinancing requires US credit history. A conventional cash-out refinance looks at your FICO score, your W-2 income, your debt-to-income ratio. If you’re outside the US, none of those exist or are relevant to a US lender.

This is where most people think the strategy stops for foreign nationals. It doesn’t.

The DSCR loan changed everything.

A DSCR (Debt Service Coverage Ratio) loan qualifies you based on the property’s income — not yours. The lender looks at one calculation:

Monthly rent ÷ Monthly PITI = DSCR ratio

(PITI = Principal + Interest + Taxes + Insurance)

Most DSCR lenders require a ratio of 1.0 or higher, meaning rent must at least cover the full mortgage payment. Premium lenders look for 1.25. If the property’s income supports the debt, you qualify — regardless of where you live, what currency your income is in, or whether you have a US Social Security number.

DSCR loans are explicitly designed for investment property. Most lenders who offer them have a foreign national program — different documentation requirements, slightly higher rates, sometimes larger down payment minimums, but the same fundamental underwriting logic: the property qualifies, not the borrower.

This is the refinance vehicle that makes BRRRR possible for foreign nationals.

What Actually Changes at Each Step

The five-step sequence works the same way. What changes is the specific tool you use at each step.

Buy: You need to purchase in an LLC — or at minimum ensure your entity structure is set up before closing. Most DSCR lenders require the property to be held in an LLC at the time of refinance. Title can sometimes transfer after rehab, but it’s cleaner to buy into the LLC from the start.

You’ll also need an ITIN (Individual Taxpayer Identification Number) to open a US bank account and receive loan disbursements. Getting an ITIN takes time — ideally handle this before you find the first deal, not after. Details in Can Non-US Citizens Buy Investment Property in the USA.

For the acquisition itself, hard money lenders are the cleanest path. Hard money is asset-based — the lender cares about the deal’s numbers, not your residency status. Rates are higher (typically 10–14%) but terms are short (6–12 months) and the approval process is fast.

Rehab: This step doesn’t change based on nationality. You need a licensed contractor you trust to manage a renovation remotely. This is a team-building problem, not a financing problem. Finding a reliable contractor is the single most important operational decision in BRRRR — and it has nothing to do with where you live.

Rent: Place a tenant through a local property manager before you refinance. Most DSCR lenders want to see an executed lease in place (or a lease that recently started). Proof of rent is what makes the DSCR math work. A vacant property can still be appraised, but you’ll have a harder time getting refinanced if there’s no demonstrated income.

Refinance: This is the critical step and where the foreign national program matters most. You’ll submit:

- Executed lease agreement

- Property appraisal (ordered by the lender)

- LLC operating agreement and articles of organization

- Foreign passport (most lenders accept this instead of a US ID)

- Proof of funds for any reserves requirement (typically 3–6 months PITI)

- Bank statements (a US account you set up via your LLC works; some lenders accept foreign accounts)

No W-2. No FICO score. No US tax returns. The lender underwrites the deal, not you.

Expect rates approximately 1–2% above what a domestic investor pays. In 2025 that puts most foreign national DSCR cash-out refinances in the 8–10% range depending on LTV, reserves, and the lender’s specific program.

Repeat: Once the refinance closes and the cash comes back, you deploy it again. Each completed cycle adds a cash-flowing hold to the portfolio. Over time, the holds generate enough passive income to fund rehab costs, closing costs, and the liquidity buffer you keep on hand — which is when the model starts feeling genuinely self-sustaining.

The Deal: Fayetteville, NC, 2021

This is deal #2 from my portfolio. The first BRRRR I ever completed.

Buy: $102,000 purchase. Distressed single-family home in a working-class Fayetteville neighborhood. The agent — investor-friendly, someone I found through a forum — assessed it as worth $165,000 ARV if properly renovated.

Rehab: $18,000 renovation. New flooring, paint, kitchen update, bathroom update. Managed entirely via contractor communication — photos, WhatsApp updates, a clear punch list. The rehab took approximately 8 weeks.

Rent: Placed a tenant at $1,400/month through a local property management company. Tenant was in place before we went to the lender.

Refinance: After-repair appraisal came in at $165,000. DSCR cash-out at 75% LTV = $123,750 loan. Monthly PITI on that loan: approximately $1,050. DSCR ratio: $1,400 ÷ $1,050 = 1.33x. The lender was comfortable. Loan closed.

The $123,750 refinance covered the $102,000 purchase and the $18,000 rehab — with roughly $3,000 left over for closing costs.

Net capital left in the deal after refinance: $0.

Monthly cash flow after PITI and property management fee: $350.

That property still generates $350/month. I have never visited it.

Common Mistakes That Break the Cycle

Buying at the wrong price. The discount on purchase is where the entire model’s math begins. If you pay full market value expecting the rehab to manufacture all your equity, the appraisal often comes back flat — meaning you can’t pull enough out in the refinance to recover your capital. The deal needs to start with a real discount.

Underestimating rehab costs. Most investors in BRRRR get burned here once. The way to avoid it: add 20% to every contractor estimate before you underwrite. If the deal still works at 120% of projected rehab cost, proceed. If it only works at the optimistic number, it’s probably not the right deal.

Refinancing too soon. Most DSCR lenders have a seasoning requirement — typically 3–6 months from purchase to refinance (some require a full year). Factor this into your holding cost projections. Hard money at 12% annual interest on a 12-month hold costs more than on a 6-month hold.

Using the wrong lender. Not all DSCR lenders have active foreign national programs. Some will quote you a loan and then decline at underwriting once they see a foreign passport and an LLC held by a non-US entity. Work with lenders who have done foreign national DSCR loans before. Ask for references from other foreign investors. The DSCR loan guide for non-US citizens has a checklist of what to ask before you apply.

Skipping the LLC. Trying to take the shortcut of buying in your personal name and transferring to an LLC before refinance sometimes triggers a due-on-sale clause in the hard money loan. Buy into the LLC from the start.

Running the portfolio without a buffer. The model has cash flowing at $350/month, but it has carrying costs too — property management, maintenance reserves, insurance, taxes. Keep 3–6 months of PITI in liquid reserves for every hold. One bad tenant or one AC unit failure will otherwise interrupt the compounding loop at the worst possible time.

FAQ

Do I need a US bank account for a DSCR loan?

Most lenders require a US account for loan disbursements. An LLC EIN lets you open a business checking account at most US banks without physically being present — Mercury, Relay, and some regional banks handle this via online application. Some lenders also accept wire receipts from foreign accounts as proof of equity, even if the loan proceeds go to a US account.

What credit score do I need?

DSCR loans for foreign nationals typically don’t use a FICO score at all, since you likely don’t have one. Lenders substitute other verification — clean bank statements, a letter from a financial institution, or in some programs, a credit report from your home country. Ask the lender specifically what they use in lieu of FICO for their foreign national program.

Can I do BRRRR without visiting the US?

Yes. Every step is executable remotely: hard money draws via wire, contractor management via video/WhatsApp, lease signing via DocuSign, appraisal managed by the lender, refinance signing via a mobile notary or US embassy. I’ve closed deals from Tel Aviv using all of these mechanisms. The team you build locally — agent, contractor, PM — is what makes remote execution possible.

What’s the minimum deal size that makes BRRRR work?

At current DSCR rates (8–10% range), you need enough ARV to generate a loan that returns your acquisition plus rehab costs. In practice, this means properties with ARVs of $130,000+ in most NC-style markets. The math gets harder in lower-value markets and easier in higher-value markets, but the ratio is what matters: buy + rehab needs to be below 75% of ARV.

How many BRRRR deals can I do simultaneously?

No limit on the number of DSCR loans a single LLC can hold. Unlike Fannie/Freddie conventional loans (which cap at 10 per entity), DSCR loans are portfolio products held by private lenders. Some lenders limit exposure per borrower at their own discretion, but the structural cap doesn’t exist the way it does in conventional financing.

The full setup — entity structure, banking, ITIN, team building, and market selection — is in How to Invest in US Real Estate from Abroad. If you want to see this strategy applied across a 24-deal portfolio built from Israel, that’s my deal history.

The Remote Investor Readiness Score will tell you where you actually stand across financing access, market selection, team building, and deal structure — based on where you are right now.

Find out exactly where you stand before your first deal.

10 questions. A personalized score across 5 dimensions. Free.

Get my readiness score →