Key Takeaways

- You do not need a US credit history, a Social Security number, or to visit the property to buy US investment real estate from abroad.

- The biggest structural barrier for foreign nationals is financing — DSCR loans solve this: they qualify on the property’s income, not yours.

- Set up your entity (LLC → EIN → ITIN → US bank account) in that order, before you start shopping for deals. Out-of-sequence setup costs money.

- Your remote team — investor-friendly agent, property manager, general contractor — is more important than any single deal. Build it before you need it.

- The REACH framework (Research → Engage → Acquire → Control → Harvest) is the repeatable system behind a $4M portfolio built across 4 US states from 7,000 miles away.

IN THIS ARTICLE

- Why everything you’ve read about this probably doesn’t apply to you

- What you actually need before deal one — the setup sequence

- Financing: why DSCR loans change everything for foreign nationals

- Research: how to find the right market from abroad

- Engage: building a remote team that works while you sleep

- Acquire: analyzing deals you’ll never visit in person

- What most people get wrong about investing in US real estate from abroad

- Frequently asked questions

- Where to start if you’re reading this for the first time

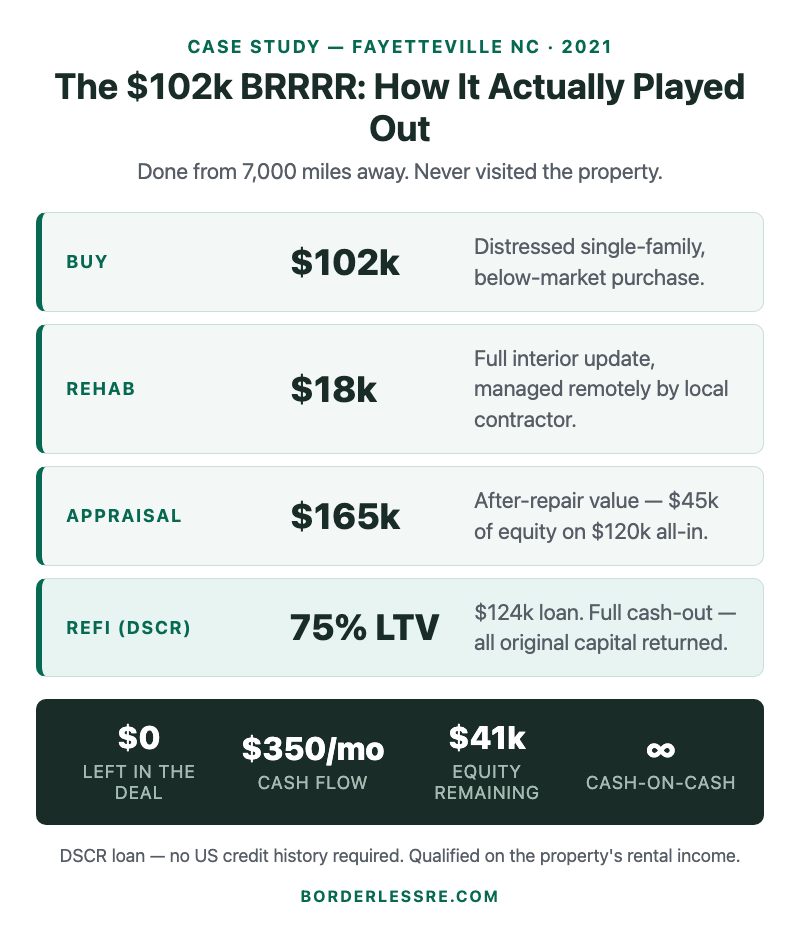

I paid $102,000 for a house in Fayetteville, North Carolina in 2021. Put $18,000 into the rehab. It appraised at $165,000. I refinanced it with a DSCR loan, pulled out all my original capital, and it still cash flows $350 a month.

I’ve never been to Fayetteville.

That was deal #2. Since then I’ve closed 22 more — across North Carolina, Florida, Georgia, and Tennessee. The portfolio is now worth around $4 million. I’ve done all of it from Israel.

This post is the guide I couldn’t find when I started. There’s no shortage of real estate investing content — but almost all of it was written by US investors, for US investors, investing in a different American state. That’s a different problem than yours. If you live outside the United States and you want to build a portfolio there, you have specific structural issues to solve that the BiggerPockets universe was not built to address: no US credit history, FIRPTA rules, time zones, wire transfers, a property manager you’ve never met in person, a lender who’s never heard of your country.

This guide covers all of it — the framework, the sequence, and the deal numbers to show it’s not theoretical.

Why everything you’ve read about this probably doesn’t apply to you

The canonical out-of-state real estate book is David Greene’s Long-Distance Real Estate Investing. It came out in 2018 and it’s genuinely good. But read the introduction: it’s written for a California investor buying in Cleveland. A US citizen with a Social Security number, an existing credit history, and the ability to fly there on a weekend if something goes sideways.

That’s not the same problem as investing from outside the country entirely.

The foreign national investor faces a different stack of challenges:

Financing. Most US mortgage products require a Social Security number, US credit history, and income that can be verified on US tax forms. If you have none of those — which you don’t if you live abroad — most lenders simply can’t help you. The product that solves this is the DSCR loan, and most OOS investing content doesn’t explain it clearly because it’s not a common product for domestic investors.

Legal structure. If you own US real estate personally as a foreign national and you sell it, the title company is required by law to withhold 15% of the gross sale price for federal taxes under FIRPTA (Foreign Investment in Real Property Tax Act). The standard fix — an LLC — is not complicated, but the setup sequence matters. Most beginners learn about FIRPTA the expensive way.

Banking. Opening a US business bank account from abroad is harder than it sounds. Most major banks require in-person visits. There are solutions, but you need to know which ones work and what documentation they actually need.

Team. An out-of-state US investor can visit their market every few months. A foreign national investor often can’t — visa constraints, cost, 12-hour flights. Your team isn’t a nice-to-have. It’s the only way this works.

None of this is insurmountable. I’ve done it 24 times. But you need a system built for your actual situation, not a domestic investing guide with the word “international” added to the title.

The system I use is called REACH.

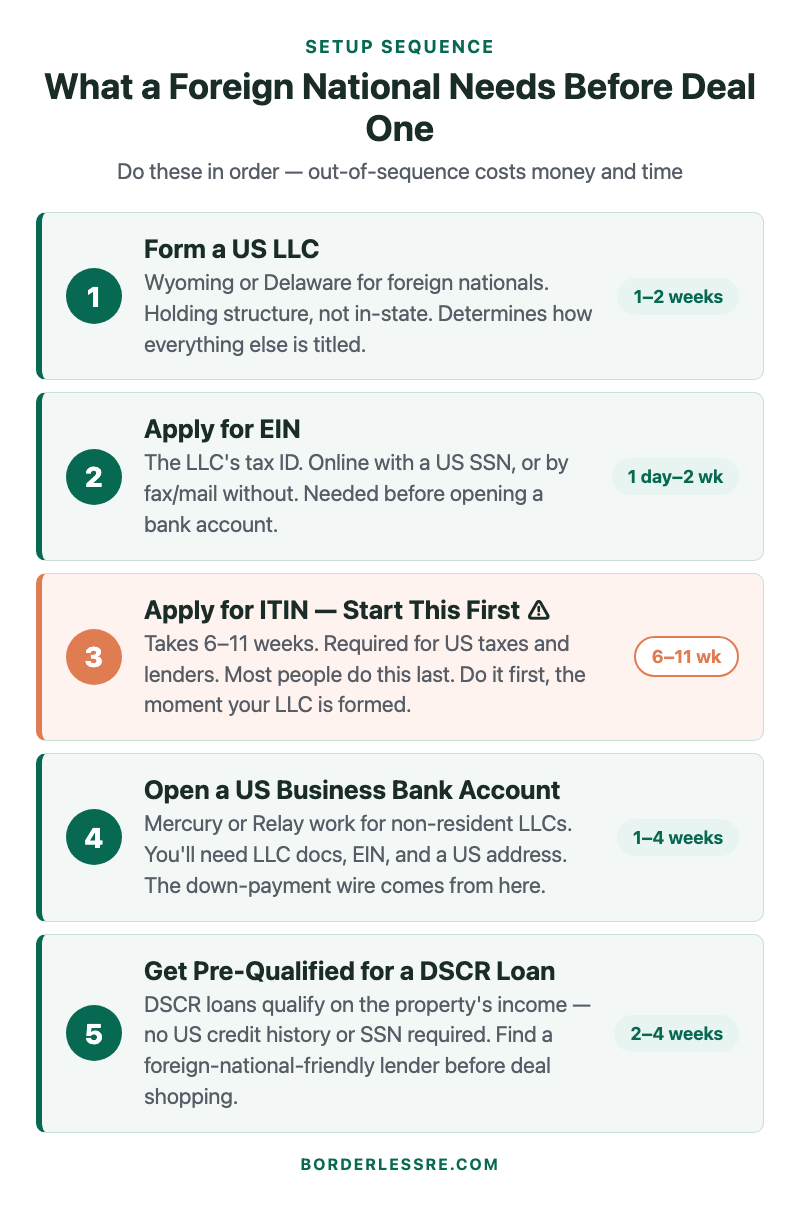

What you actually need before deal one — the setup sequence

This is where most foreign national investors go wrong. They start shopping for deals before the structural foundation is in place. Then they find a deal they love, and the closing timeline collapses because the bank account isn’t open, or the ITIN is still pending, or the lender needs LLC docs they don’t have.

The sequence matters. Do it in this order:

1. Form a US LLC. Not a personal purchase — an LLC. Wyoming and Delaware are the most common choices for foreign nationals; both allow non-resident ownership and have low annual costs. This is the entity your properties will be titled in. Everything else depends on getting this right first.

2. Get your EIN (Employer Identification Number). This is the LLC’s tax ID. You need it before you can open a business bank account. US citizens can get it instantly online. If you don’t have a US SSN, you apply by fax or mail — plan for 2–4 weeks.

3. Apply for your ITIN (Individual Taxpayer Identification Number). Start this the moment your LLC is formed. ITIN applications for foreign nationals take 6–11 weeks at the IRS. You’ll need it to file US taxes on rental income — and some lenders require it. This is the step most people do last. Do it first.

4. Open a US business bank account. Mercury and Relay are the most reliable options for non-resident LLCs as of 2026. Both can be done online without a US visit. You’ll need your LLC documents, EIN, and a US registered agent address. This is the account your down payment wire will come from when you close.

5. Get DSCR pre-qualified. Before you start seriously shopping for deals, talk to a foreign-national-friendly lender. Understand what they’ll lend on, at what LTV, with what reserve requirements. Pre-qualification doesn’t commit you to anything — it tells you your budget and removes the financing question from the deal analysis.

Financing: why DSCR loans change everything for foreign nationals

A DSCR loan (Debt-Service Coverage Ratio loan) qualifies you based on the property’s income, not your personal income. The lender looks at one ratio:

DSCR = Monthly rental income ÷ Monthly debt payment (PITI)

If that ratio is 1.0 or higher, the property covers its own debt. Most lenders want to see 1.1–1.25 on a DSCR loan. A property renting for $1,400/month with a mortgage payment of $1,200 (principal, interest, taxes, insurance) has a DSCR of 1.17 — that’s typically approvable.

What this means for you as a foreign national:

- No SSN required. DSCR lenders work with ITINs and, in some cases, foreign passports.

- No US credit history required. The underwriting is on the property, not on you.

- No income verification. Your salary, your foreign tax returns, your employment situation — irrelevant to the lender.

The tradeoffs: DSCR loans typically require 20–30% down (vs. 15–20% for conventional), and rates are 0.5–1.5% higher than conventional investment property loans. On a $175,000 purchase that’s roughly $44,000–$52,000 down.

The 2023 NAR International Transactions in US Residential Real Estate report shows that foreign buyers purchased $53.3 billion in US residential property in 2023. Most of them don’t have US credit histories. The DSCR product exists specifically because lenders figured out how to qualify on the asset, not the borrower.

On the Fayetteville deal, the refinance was a DSCR cash-out. The property rented for $1,350/month. The DSCR loan at 75% LTV on a $165k appraisal was $124k. At that balance, the monthly payment was roughly $950 (PITI). DSCR of 1.42. Approved without a US credit history, without an SSN, from 7,000 miles away.

Research: how to find the right market from abroad

I made my worst market decision in 2021. I bought a property in Cleveland, Ohio — partly because a turnkey company was marketing it hard, partly because the numbers looked fine on a spreadsheet. The market had a landlord law issue I didn’t understand, the neighborhood was more C-class than I’d been told, and the property management situation was a disaster. I exited with a small loss.

The mistake wasn’t that I bought from abroad. The mistake was that I didn’t do the market selection work before I talked to a single deal source.

Markets matter more than deals. A mediocre deal in a good market outperforms a good deal in a bad market almost every time. Here’s what I look for before I’ll consider any market:

Landlord-friendly laws. Can you evict a non-paying tenant in under 60 days? Some states (California, Illinois, New York) have eviction processes that can stretch 6–12 months. As a remote investor, a bad tenant in an unfavorable legal environment is an expensive problem you can’t easily solve from abroad. North Carolina’s eviction process runs 30–45 days in most cases. That’s a structural advantage I’m not willing to give up.

Price-to-rent ratio. A rough benchmark: monthly rent should be at least 0.8–1% of the purchase price. A $150,000 house renting for $1,300/month is at 0.87% — workable. The same house renting for $950 in a coastal market is at 0.63% — hard to make cash flow without significant appreciation dependence.

Population and job base. Markets with military installations, universities, or healthcare campuses have stable tenant demand. Fayetteville has Fort Liberty (formerly Fort Bragg). You want tenants who are going to be there, and you want a tenant base that doesn’t disappear when one employer leaves.

Supply constraints. This is about your exit, not your entry. Can the market absorb new supply that competes with your units, or is zoning and land constraint keeping inventory tight?

North Carolina has been my primary market since 2020. It checks every box. I’ve also bought in Florida and Georgia for similar reasons.

Engage: building a remote team that works while you sleep

The team is everything. A deal without a team isn’t an investment — it’s a liability.

The three people you need in place before you buy your first property in any market:

An investor-friendly real estate agent. Not someone who sells houses to families. Someone who thinks in ARV, understands off-market sourcing, is comfortable with investors who will never set foot in the property, and has connections to deals before they hit the MLS. Ask them: “How many investment transactions did you close last year?” If the answer is under 10, keep looking.

A property manager. Your boots on the ground. They handle tenant screening, rent collection, maintenance calls, and the 11pm emergency plumbing situation. They are your eyes. Interview three before you choose one. Ask for references from current investor clients — not testimonials, actual clients you can call. Ask about their vacancy and eviction track records. A bad PM is more expensive than a bad deal.

A general contractor. You will never be able to visit a property during a rehab. Your contractor has to be trustworthy enough to execute a scope of work with a budget and a timeline, communicate via video walkthroughs, and flag problems before they become expensive. The first time you work with a new contractor, keep the scope small — see how they handle a $10k job before you hand them a $50k rehab.

Never buy in a market where you don’t have all three of these in place. If the deal comes before the team, you’re not ready for that market yet.

Acquire: analyzing deals you’ll never visit in person

The analysis is the same whether you live 20 miles from the property or 7,000. The process for remote due diligence is different.

On the analysis side, I look at five numbers before I look at anything else:

- Purchase price vs. ARV. What’s the spread? For a BRRRR, I want to buy at 65–70% of ARV before rehab costs. If the ARV is $165k, I want my all-in cost (purchase + rehab) to be under $115k.

- Monthly rent vs. PITI. Will the property cash flow after a DSCR refinance? Model the post-refi payment, not the acquisition.

- Vacancy rate. I assume 8% vacancy on all deals. If the market is tighter, great. If it’s not, I’m covered.

- Property management fee. Usually 8–12% of monthly rent. I underwrite at 10%, always, even if the PM quotes me 8.

- Capex reserve. I set aside 8% of monthly rent for capital expenditures — roof, HVAC, plumbing. Remote investors get surprised by capex more than local investors because they’re not seeing the property age in person.

On the due diligence side, remote doesn’t mean blind. It means:

- Video walkthrough from your agent before making an offer

- Home inspection from an independent inspector you’ve vetted (not referred by the listing agent)

- Video walkthrough from your contractor before closing, with a line-item scope and budget

- Title insurance, always

The Fayetteville deal took me four hours of analysis and one video call with my contractor. That’s it.

What most people get wrong about investing in US real estate from abroad

“You need to visit before you buy.”

You don’t. I’ve never visited most of the properties I own. The visit is a comfort mechanism, not a due diligence mechanism. A thorough remote due diligence process — independent inspector, contractor walkthrough, video from your agent — gives you more actionable information than an in-person visit where you’re looking at paint colors and cabinet handles. The professionals you’ve hired have seen hundreds of properties. You haven’t. Trust their eyes, verify their reports.

“Start with cash flow.”

Cash flow is the output, not the strategy. A $150,000 property generating $250/month net cash flow has a 2% cash-on-cash return. That’s not wealth building — that’s a very illiquid savings account. The strategy is equity accumulation: buy below value, add value through rehab, refinance at the new value, redeploy the capital. Cash flow follows naturally once you’ve built the equity base. Chasing cash flow from day one pushes you toward C-class neighborhoods and C-class tenants — the most management-intensive segment of the market, which is exactly where you don’t want to be when you’re 7,000 miles away.

“Wait until the market settles / rates come down / timing is right.”

The information is infinite. You will always be able to find a reason to wait. My first deal was in 2020, when rates were 3.5% and everyone thought COVID would destroy real estate. My fifth was in 2022 when rates were at 7% and everyone thought the market was crashing. The framework doesn’t change with rates — you underwrite at current rates, you buy at current prices, you adjust your deal criteria accordingly. Waiting for a perfect market is a choice to stay on the sideline indefinitely.

Frequently asked questions

Can a foreign national own US real estate directly, or do they need an LLC?

Technically, you can own US real estate personally as a foreign national — there’s no law against it. In practice, you almost certainly shouldn’t. Owning personally exposes you to FIRPTA withholding (15% of gross sale price when you sell), personal liability, and a less efficient tax structure. An LLC held by a foreign national or a foreign corporation is the standard approach. Talk to a US CPA with foreign national real estate experience before you buy anything.

What is FIRPTA and how does it affect me as a foreign seller?

FIRPTA (Foreign Investment in Real Property Tax Act) requires title companies to withhold 15% of the gross sale price when a foreign national sells US real estate and remit it to the IRS. This is a withholding on the sale price, not the gain — which means on a $200,000 sale, $30,000 gets withheld regardless of what you paid or what your actual tax liability is. You get it back when you file your US tax return if your actual tax owed is less. The standard protection is to sell through an LLC structure where the withholding rules are different, and to work with a CPA who knows the rules. This is not a reason to avoid US real estate — it’s a reason to set up your structure correctly before you buy.

Do I need to come to the US to close on a property?

No. Remote closings are standard in most US states. You sign documents via notarized e-signature or through a US-based signing service. Your down payment and closing costs are wired from your US business bank account. I have never attended a closing in person for any of my 24 deals.

How do I handle taxes on US rental income as a foreign national?

Foreign nationals who earn rental income from US real estate must file a US tax return (Form 1040-NR for individuals; the LLC files its own return depending on structure). You’ll need an ITIN to file. Your rental income is subject to US federal income tax after deductions (depreciation, mortgage interest, repairs, PM fees, etc.) — which often reduces your taxable income significantly in the early years. You’ll also need to consider how your home country treats this income. Most countries with US tax treaties allow foreign tax credits to prevent double taxation. This is a real compliance obligation; get a qualified CPA from day one.

How do I find a lender who will actually work with foreign nationals?

Start with lenders who specifically advertise DSCR loans for foreign nationals — not every DSCR lender takes foreign national borrowers. Search for “DSCR loan foreign national investor” and look for lenders who explicitly list foreign national programs. Expect to provide your passport, ITIN (or pending application), LLC documents, proof of rental income from the subject property (the lender orders an appraisal with a rental schedule), and 3–6 months of US bank account reserves. Interest rates and LTV limits vary by lender and are negotiable based on your reserve position.

What happens if something goes wrong with the property while I’m 7,000 miles away?

This is the right question to ask, and the answer is: your team handles it. Your property manager is the first call when the HVAC fails, a tenant doesn’t pay, or there’s water damage. Your PM should have a pre-authorized maintenance limit (typically $200–$300) below which they handle issues without calling you. Above that limit, they contact you, get approval, and coordinate the contractor. The PM is why you can be in a different time zone and not panic every time something breaks. Choose the PM carefully — this person is more important than any individual deal.

Where to start if you’re reading this for the first time

The single most useful thing you can do right now is figure out where you actually stand.

Not in a general “do I have capital” sense. In a specific, diagnostic sense: How ready are you across the five dimensions that actually matter — capital, legal setup, financing access, market and deal knowledge, and team? Which one is your bottleneck?

Most people don’t know the answer to that question. They think it’s capital when it’s actually team setup. Or they think it’s knowledge when it’s actually financing. The bottleneck determines the next step — and the next step is different for everyone.

I built a free, 10-question assessment that gives you a score across all five dimensions and identifies your specific gap. It takes 3 minutes. The result tells you where you stand and what to close first.

Get your Remote Investor Readiness Score →

If you’re not quite there yet and want the step-by-step sequence first, the First Deal Roadmap covers the 7 steps in the order that matters — with what I actually did at each stage.

The information is here. The question is where you are in it.

Roy Gottesdiener has built a $4M US real estate portfolio across 4 states since 2020, entirely from Israel. He’s never visited most of the properties he owns.

Find out exactly where you stand before your first deal.

10 questions. A personalized score across 5 dimensions. Free.

Get my readiness score →