Key Takeaways

- The single biggest reason out-of-state real estate goes sideways isn’t the market — it’s the property manager. A bad PM can turn a $400/month cash flow property into break-even by year two and you won’t notice until the damage is done.

- I lost real money on five Cleveland properties between 2021 and 2026 mostly because the PM I hired was reactive, not proactive. The properties weren’t the problem. The operator was.

- I now use a 5-question interview, one specific contract clause that most PMs resist, and a verification process that involves calling current owner-clients I find independently — not the references the PM offers.

- The system below works the same whether you’re a US investor in California buying in Indianapolis or an international investor in Tel Aviv buying in North Carolina. Distance is distance.

- Bad PMs are easy to spot once you know the pattern. The hard part is being patient enough not to hire the first one who answers the phone.

IN THIS ARTICLE

- How to Find a Property Manager Out of State Without the Cleveland Mistake

- Why the PM Decision Is the Whole Game (and Why You Probably Underrate It)

- The 5 Questions I Ask Every PM Before Signing Anything

- The One Contract Clause Most PMs Resist (and Why You Insist On It)

- How to Verify a PM (And Why Their Reference List Doesn’t Count)

- Red Flags and Green Flags: The Pattern I Wish I’d Recognized in 2021

- What Most People Get Wrong About Vetting Property Managers Remotely

- Frequently Asked Questions

How to Find a Property Manager Out of State Without the Cleveland Mistake

The honest version of how to find a property manager out of state is this: most of the work happens before you talk to a single PM. The mistake is treating PM selection like vendor selection. It isn’t. The PM is the operating partner who decides which tenants live in your property, how fast turnovers happen, whether maintenance gets caught early or late, and whether your deal economics actually survive year two. Wrong PM, wrong outcome, regardless of how good the property is.

I’m writing this post because I’ve been the investor who got it wrong. In 2021 I bought five single-family BRRRRs in Cleveland and hired one PM to manage all of them. The PM had decent reviews, returned my calls, sounded competent on the phone. None of that was the problem. The problem was that he was reactive — he handled issues as they came in, but never went looking for them. By the time I had data showing the system wasn’t working, I was already 18 months and several tenant cycles deep. I exited all five Cleveland properties between 2023 and 2026 at break-even or small losses. The cost of the PM mistake was in the same ballpark as the cost of the market mistake. I’m not sure the property cluster would have failed with a different operator.

This post is what I do now. Five vetting questions. One contract clause. A verification process. A red-flag list. The system works the same whether you live in California buying in Cleveland or in Tel Aviv buying in North Carolina — the friction of distance is identical, the math of a bad PM is identical, the recovery cost is identical. If you’re new to out-of-state real estate investing, this is the first piece of infrastructure you build. Not the property. The team.

Why the PM Decision Is the Whole Game (and Why You Probably Underrate It)

Most investors spend more time analyzing properties than vetting PMs. That ratio is backwards. A property is a fixed thing — its numbers are either there or they aren’t, and you can model them with a spreadsheet. A PM is a relationship that compounds over years and shapes every operational outcome the property produces. The numbers on the spreadsheet assume the operator behaves a certain way. The operator usually doesn’t.

Here’s what a bad PM costs, in concrete terms. Tenant placement matters most: a marginal tenant placed quickly to fill a vacancy can cost $5k–$15k in damages, missed rent, and eviction fees if it goes wrong. Maintenance latency: a leak caught early costs $300; the same leak caught after the ceiling drywall fails costs $4,000. Turnover speed: every extra week of vacancy on a $1,400 rent unit is roughly $325 of cash flow gone, and a bad PM routinely runs 3–6 weeks longer turnover than a good one. Across a 12-month period, the difference between a top-quartile PM and a bottom-quartile PM on the same property is realistically $4,000–$8,000 in net operating income. That’s not a small variance — it’s the difference between a property that compounds and a property that drags.

For remote investors specifically, the cost is higher because you can’t physically check on anything. The US-domestic OOS investor in another state can drive over once a quarter to see things in person. The international investor can’t. Either way, you’re trusting the PM’s reporting to be accurate, and a PM who is sloppy or incentive-misaligned will hide problems either by intent or by inattention. The PM is the operational firewall between you and the property. The firewall has to be solid.

The thing most investors get wrong is hiring the first PM who returns their call. Returning calls is the lowest possible bar. The PMs worth working with are also the ones who turn down work — they have a thesis about which properties they’ll manage, which markets they operate in, and what kind of investor they fit with. A PM who will manage anything for anyone is usually a PM with too much capacity, which usually means they have a retention problem.

The 5 Questions I Ask Every PM Before Signing Anything

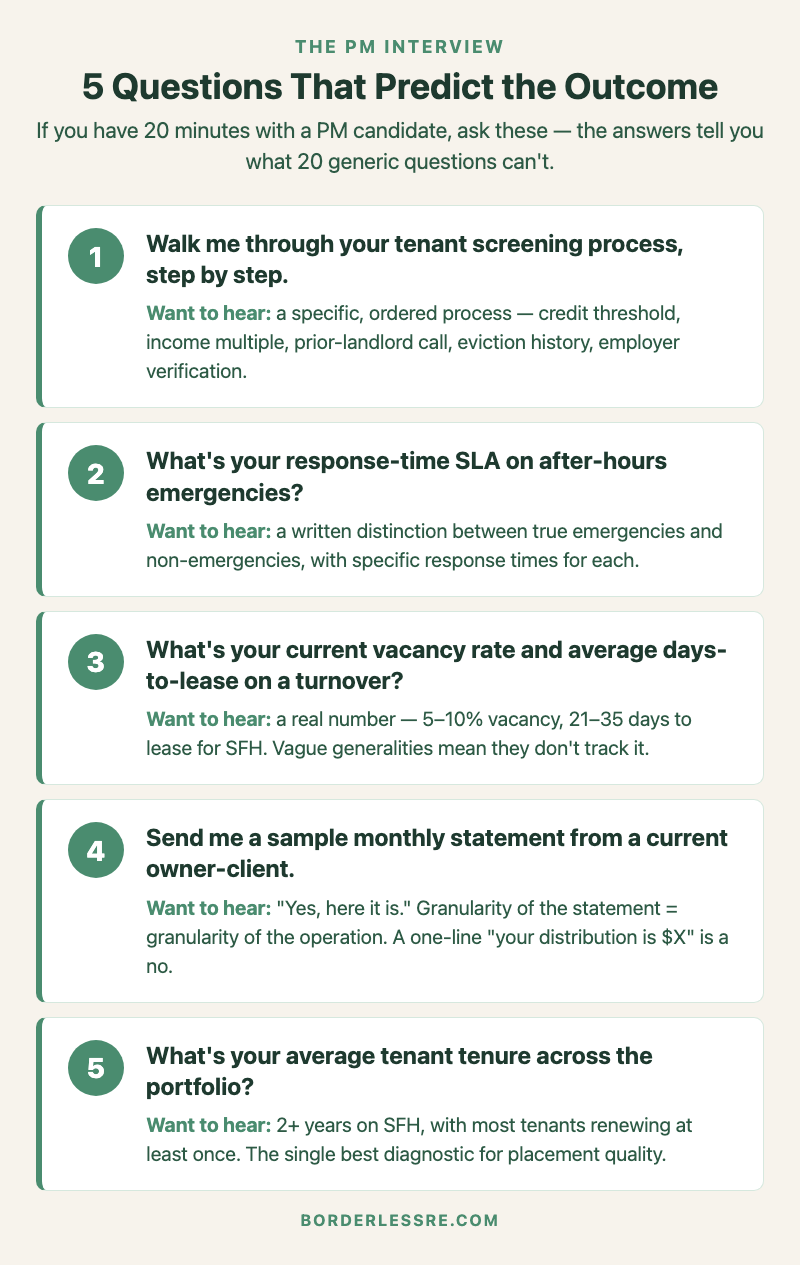

Generic PM-vetting articles usually give you 20+ questions. Most of them don’t matter. The five below are the ones whose answers actually predict outcome. I’ve asked these of every PM I’ve engaged since Cleveland, and the answers have correctly screened out the operators who would have cost me money. If you’re choosing between PMs and you only have 20 minutes, ask these.

Question 1: Walk me through your tenant screening process, step by step. What I want to hear: a specific, ordered process. Credit pull above X, income verification at Y multiple of rent, prior landlord reference call (not just contact info — they actually call), eviction history check across multiple jurisdictions, employment verification with the employer directly. What I don’t want to hear: “we use TransUnion SmartMove” with no further detail. The platform isn’t the screen — the policies and judgment around it are. A PM who can’t articulate a thoughtful tenant policy is a PM who places marginal tenants under pressure.

Question 2: What’s your response-time SLA on after-hours emergency calls, and what does “emergency” actually mean to you? What I want to hear: a clear distinction between true emergencies (no heat in winter, no water, electrical hazards, security breaches) and non-emergencies, with a specific commitment on response time for each. Bonus points for a 24/7 answering service that actually escalates to a human, not a voicemail. What I don’t want to hear: “we get back to people as fast as we can.” That’s not a policy.

Question 3: What’s your current vacancy rate across the portfolio, and what’s your average days-to-lease on a turnover? What I want to hear: a real number, in the 5–10% vacancy range and 21–35 days to lease for typical SFH inventory. PMs who quote 0% vacancy are either lying or so small they have no statistical sample. PMs above 15% vacancy or 60+ days to lease have an operational problem they’re not solving. What I don’t want to hear: vague generalities or “varies by market.”

Question 4: Send me a sample monthly statement — same format you send your current owner-clients. What I want to hear: a clean, line-itemed statement showing rent collected, all expenses with vendor name and date, reserve balance, and YTD running totals. Bonus points if there’s a portal where I can see invoices and pay stubs in real time. What I don’t want to hear: a single-line “your distribution this month is $X” with no detail. The granularity of the statement is a near-perfect proxy for the granularity of the operation.

Question 5: What’s your average tenant tenure across the portfolio? What I want to hear: 2+ years on SFH, with most tenants renewing at least once. This is the single best diagnostic for whether the PM is placing the right tenants in the first place and treating them well enough that they want to stay. What I don’t want to hear: anything under 18 months (which means constant turnover, expensive on every metric) or “I haven’t tracked that” (which means the PM doesn’t run their business on data).

The PMs who answer all five well will also be the ones with capacity to take you on. The PMs who can’t answer them are the ones with availability — for the wrong reasons.

The One Contract Clause Most PMs Resist (and Why You Insist On It)

Standard property management agreements are written by the PM, for the PM. They include the standard terms: management fee (8–12%), leasing fee (50–100% of one month’s rent), maintenance markup, mandatory minimum reserves. Most of those are reasonable industry terms.

The clause I insist on adding — and that most PMs initially resist — is a maintenance approval threshold for any single repair above a fixed dollar amount, with written documentation required. My current threshold is $500. Anything below $500, the PM can authorize and bill against the reserve account without my approval. Anything at or above $500, the PM must email me with the issue, the proposed scope, the bid, and the timeline, and wait for written approval before proceeding.

Why this matters: without the clause, a PM with a wide brush can rack up $4,000–$6,000 of maintenance in a month against your reserves, none of which you signed off on, all of which is technically allowed by the standard agreement. The PM gets the markup. You get the bill. Your cash flow disappears and you can’t push back without seeming difficult — because you signed the agreement that gave them the authority. With the clause, every meaningful expense passes through your inbox first. It takes a few minutes per month and it saves real money.

PMs resist the clause for two reasons. The honest one: it slows them down on emergency repairs. The fix is to build in an exception for true emergencies (water leak active, heat out in winter, etc.), where the PM can act immediately and notify you within 24 hours after. The less-honest reason: the PM makes margin on maintenance markups and the clause reduces their take. That’s not an argument against the clause — that’s a reason for it.

The PM who refuses the clause outright is telling you something important. Either they don’t trust their own judgment enough to want it documented, or they’re protecting a revenue stream that depends on you not paying attention. Both are reasons to keep shopping. I’ve never had a PM I want to work with refuse this clause once we discussed why I wanted it. PMs who fight the clause aren’t the PMs you want.

How to Verify a PM (And Why Their Reference List Doesn’t Count)

The reference list a PM gives you is a curated marketing asset. They picked the three owners who would say nice things about them. The verification you actually need is the verification they didn’t curate.

Here’s the process I use:

- Pull permits in the PM’s name from the county records database. Most counties make this public online. Look at the volume and type of work the PM has been involved with over the last 12–24 months. A PM whose permits are mostly small repairs at the same handful of properties isn’t running a real portfolio — they may have a few properties they manage well and not much else. A PM with diversified permit history across different owners is operating at scale.

- Search BiggerPockets, Reddit, and local landlord Facebook groups for the PM’s name. If a PM has been in business for 5+ years in a market, they have a public reputation. Investors talk. The complaints are usually specific (slow turnover, high maintenance markups, missed rent collection) and they recur across multiple posters. One bad review is signal noise; three saying the same thing is signal.

- Find current owner-clients independently and call them. This is the step most investors skip and it’s the most valuable. Pull recent property transfers in the PM’s market through county records or Zillow’s “recently sold” filter. Call the new owners cold. Ask: “I’m researching property managers in [market]. Can I ask who you use and what your experience has been?” About 25% of cold calls answer the question honestly. Three honest answers from three random current investors tells you more than thirty curated references.

- Drive the portfolio if you can; have someone else drive it if you can’t. A PM’s portfolio condition is their resume. If the houses look maintained from the curb — yards mowed, no obvious deferred maintenance — that says something real about how the PM operates. If you can’t go in person, hire a local home inspector for $250 to drive by 5–6 of the PM’s properties and send you photos. It’s the cheapest verification money you’ll ever spend.

- Talk to a contractor in the same market who works with multiple PMs. Local GCs and trades have direct visibility into how PMs operate — who pays on time, who lets work pile up, who runs scope creep on owner accounts. A 15-minute call with a contractor who works with 5+ PMs in the market will surface things no reference call ever will. Your real estate agent can usually make the introduction.

The total time on this verification is 4–6 hours. The PMs who survive it are the PMs worth a 12–24 month commitment. The PMs who fail any single step are not worth your capital.

Red Flags and Green Flags: The Pattern I Wish I’d Recognized in 2021

After Cleveland, I went back through the original interview transcripts with the PM I hired and circled the warning signs. They were all there. I just didn’t know what I was looking at. Below is the pattern I now use to triage PM candidates fast.

The red flags, in order of how predictive they are:

- Vague answers to specific operational questions. A PM who can’t articulate their tenant screening process in 60 seconds doesn’t have one. A PM who can’t quote their current vacancy rate doesn’t track it. A PM who answers “we handle all of that” without specifics is hoping you don’t ask follow-ups.

- Refusing the maintenance approval clause without offering a reasonable alternative. Already covered above. This one is binary.

- Pressure to sign quickly. A good PM has a waitlist. They don’t need your $1,200/month management fee badly enough to push you. A PM who wants the agreement signed this week is a PM with capacity problems they’re not telling you about.

- No portal, paper-only reporting. This isn’t about technology nostalgia — it’s about transparency. A PM who can’t show you a real-time portal in 2026 is a PM whose accounting you have to take on faith. Don’t.

- Consistently negative tone about tenants. PMs who refer to tenants as “they” and complain about them across the conversation tend to place tenants who reflect that attitude. Tenant outcomes are downstream of how the PM thinks about tenants. A PM who treats tenants like a problem will manage your property like a problem.

The green flags that predict good outcomes:

- Pushback on something specific in your model. A good PM has opinions. If they review your projected pro-forma and say “your turnover assumption is too low for that submarket,” that’s a green flag — they know their market and they’re willing to disagree with you. PMs who agree with everything you say are PMs who will tell you what you want to hear when problems arise.

- A waitlist, or a careful intake process. PMs who screen owners as carefully as they screen tenants are PMs whose portfolios run cleaner because they’re not mixing incompatible owner expectations. You should have to qualify to work with them.

- Specific data when asked. Not just average vacancy — vacancy by submarket, by property type, with year-over-year comparison. PMs who run their business on data are PMs whose data you can trust.

- Written escalation policy. They’ve thought about what counts as an emergency, what counts as a 24-hour response, what counts as a routine repair, and they can show it to you in writing.

- Tenure of their own staff. Ask how long their current leasing manager and head property manager have been with the company. Long-tenure staff means the operating system is stable. High-turnover staff means problems compound at the personnel level before they show up at the portfolio level.

What Most People Get Wrong About Vetting Property Managers Remotely

The conventional advice on PM vetting is dominated by two failure modes — both of which contributed to my Cleveland mistake.

Failure mode 1: Optimizing for management fee percentage. Investors comparison-shop PMs the way they comparison-shop airfare, focusing on the headline 8% vs. 10% management fee. This is almost completely the wrong axis. A 10% PM who runs 4-week turnovers and screens tenants well will outperform an 8% PM who runs 8-week turnovers and places marginal tenants by an order of magnitude on net cash flow. Two extra points of management fee on a $1,400/month rent is $336/year. A single placed-then-evicted bad tenant is $5,000+. The fee is a rounding error compared to the outcomes the PM produces. Pay the right PM their fee. Don’t shop the cheapest one.

Failure mode 2: Trusting size and longevity as proxies for quality. Big established PMs in established markets often have the worst owner outcomes because the senior people who built the operation aren’t running it anymore — newer junior staff are, and the systems haven’t kept up with the volume. The right PM for a remote investor is usually a mid-size operator (200–500 doors, not 50, not 5,000) with the founder still actively involved. Big enough to have systems, small enough that the systems haven’t decayed.

Failure mode 3 (the one I made): Hiring quickly to match the property purchase timeline rather than the PM vetting timeline. I bought the first Cleveland property and gave myself a week to find a PM. That’s not a vetting process — that’s a checkbox. The right sequence is: build the team first, then buy the property the team can manage. I now spend 4–8 weeks on PM vetting in any new market before I’ll close on a property there. The deal that requires you to skip the vetting is the deal that costs you the most. There will be another deal. There may not be another chance to set up the team correctly before this one closes.

The international-investor specific failure mode worth flagging: assuming the PM understands the constraints of working with a non-resident owner. Most don’t. They’ve never had to coordinate a wire from a foreign bank account, never had to handle 1099 reporting for a foreign-owned LLC, never had to run a translation when the tenant complaint is in Spanish and the owner is in Israel. Ask explicitly during the interview whether they’ve worked with foreign-owned LLCs. If they haven’t, it’s not necessarily a deal-breaker, but it raises the cost of the relationship — you’ll be teaching them as you go, which is fine if they’re teachable and a problem if they’re not.

Frequently Asked Questions

How much should I pay a property manager?

For single-family rentals, expect 8–12% of monthly rent collected as the management fee, plus a leasing fee of 50–100% of one month’s rent on tenant placement, plus a smaller renewal fee (often 25% of one month’s rent or a flat $100–200). Maintenance markup of 10% is standard. Headline fees vary; total cost of ownership is what matters. A 10% PM who keeps your unit rented and runs clean turnovers is cheaper than an 8% PM who doesn’t.

What’s the biggest red flag when interviewing a property manager?

Vague answers on tenant screening. The PM’s tenant policy is the most consequential thing they do — it determines who lives in your property, how they pay, how they treat the unit, and how long they stay. A PM who can’t articulate their screening process in 60 seconds with specifics doesn’t have one. Walk away.

Should I use a small or large property management company?

Mid-size operators (200–500 doors) usually produce the best outcomes for remote investors. Small operators (under 100 doors) are often single-person operations with capacity risk and limited bench depth. Large operators (1,000+ doors) tend to have decayed systems where the people who built the company aren’t running it anymore. Mid-size, with the founder still involved, hits the sweet spot.

How long should I lock in a property management agreement?

I sign for 12 months with a 30-day termination clause that’s mutual and doesn’t require cause. Anything longer than 12 months without a clean exit clause is a PM protecting their revenue, not a PM serving you. Anything shorter than 12 months means the PM hasn’t had enough time to demonstrate operational consistency through at least one full tenant cycle.

Can I manage my rental property remotely without a property manager?

Technically yes, especially for short-term or mid-term rentals where guest turnover is on you anyway. For long-term rentals at scale, self-management remotely is mostly a worse deal than hiring well — your time is more valuable than the 8–12% you’d save, and the operational complexity (lease enforcement, evictions, maintenance dispatch across time zones) eats whatever margin you thought you were capturing. The exception is investors with 1–3 properties in a single market they visit regularly. At 4+ properties or true remote operation, hire a PM.

Do I need a different property manager if I’m a foreign investor?

Not always, but you need a PM who has at least seen a foreign-owned LLC before. Ask during the interview: have you worked with non-resident owners? Do you understand the wire mechanics of distributions to foreign banks, the 1099 reporting requirements, and the FIRPTA implications on exit? A PM who hasn’t can be educated, but it’s a higher-cost relationship than a PM who already knows the playbook. The full setup picture for international investors is in how to invest in US real estate from abroad.

So how do you find a property manager out of state without getting burned? Slow down, ask the five specific questions above, insist on the maintenance approval clause, verify the PM independently of the references they offer, and walk away from anyone who pushes you to sign quickly. The PM decision compounds for years. The vetting is the cheapest insurance you’ll ever buy on a property.

If you’ve taken the Remote Investor Readiness Score and your Team Setup dimension came back weak, this is the post you act on first. The score doesn’t tell you how to fix it — that’s what this is for. Five questions, one clause, four verification steps. Build the team first. Then go find the deal. The deal can wait. The team takes the time it takes, and the time it takes is what makes the deal work.

Find out exactly where you stand before your first deal.

10 questions. A personalized score across 5 dimensions. Free.

Get my readiness score →