Key Takeaways

- Non-US citizens can legally buy investment property in America — no restrictions

- You don’t need a US Social Security number, credit history, or US residency

- You need five things in a specific sequence: LLC → EIN → ITIN → US bank account → DSCR pre-qualification

- ITIN takes 6–11 weeks — start it immediately when you form the LLC, not when you find a deal

- DSCR loans qualify on the property’s rental income, not your personal income or credit history

- Total setup cost: roughly $2,000–5,000 one-time, before your first deal

Yes. You can buy investment property in the USA as a non-US citizen.

There’s no law preventing it. No residency requirement. No citizenship requirement. Foreign nationals have the same property ownership rights in America as US citizens, and I’ve exercised those rights 24 times — every single deal closed while I was sitting in Tel Aviv.

The real question isn’t whether you can. It’s what you need in place before you try.

That list is shorter than you think. But the sequence matters.

What You Actually Need

Five things. In this order:

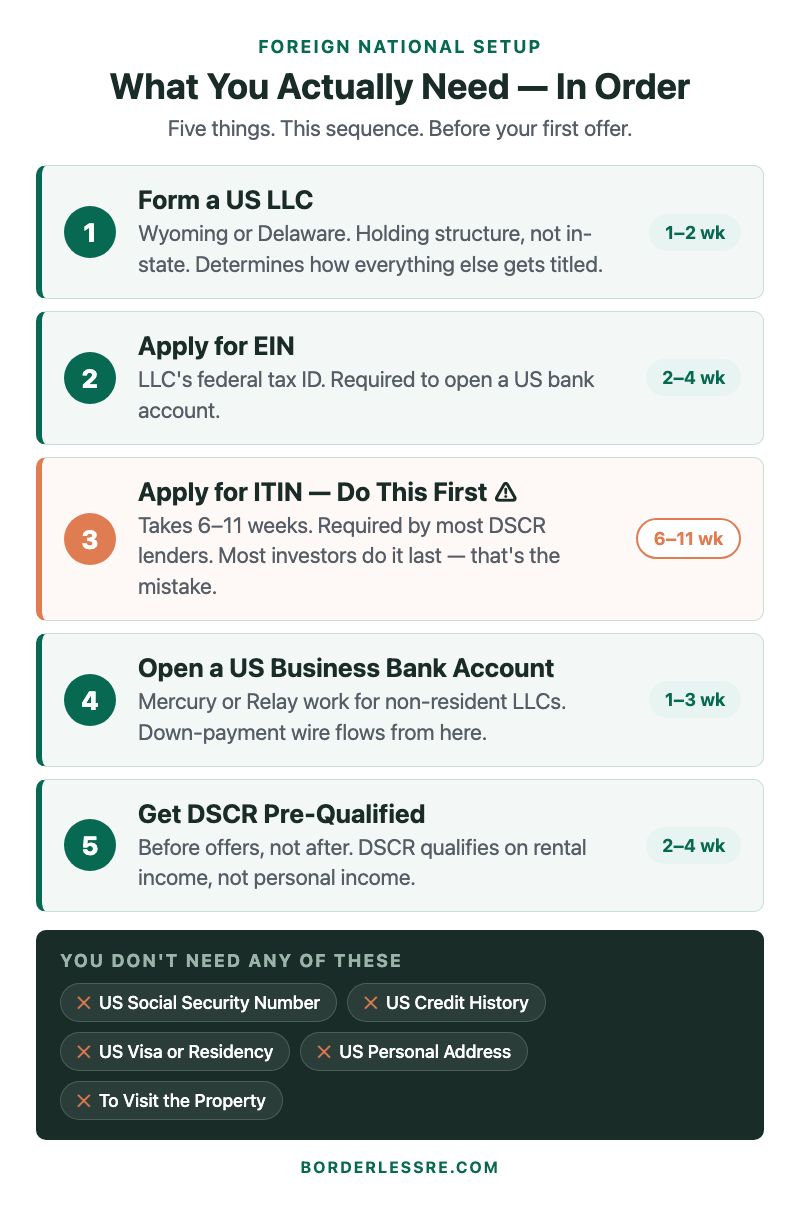

1. A US LLC

Wyoming or Delaware — not in your investment state. This determines how everything else is titled: the property, the loan, the bank account. Do this before anything else.

2. An EIN

The LLC’s federal tax ID. You need it to open a bank account and to operate as a business entity. If you don’t have a US Social Security number, you apply by fax or mail — takes 2–4 weeks.

3. An ITIN — start this immediately after the LLC

The ITIN is your individual US tax identification number. It’s what lets you file US taxes as a non-resident, and what most DSCR lenders require. The IRS processes ITIN applications in 6–11 weeks. Most investors do it last. That’s a mistake — I’ll explain why below.

4. A US Business Bank Account

Mercury and Relay both work for non-resident LLCs. You’ll need your LLC formation documents, EIN, and a US registered address. This is where your down payment wire comes from when you close a deal.

5. DSCR Loan Pre-Qualification

Get pre-qualified before you start making offers — not after you find a property. DSCR loans don’t require US credit history or a Social Security number. They qualify on the property’s rental income. But you want to know your parameters before you’re in contract with a 21-day close window.

What You Don’t Need

This list surprises most people.

A US Social Security number. Not required for investment property ownership or for DSCR financing.

A US credit history. Irrelevant for DSCR loans. The lender is evaluating the property, not your credit file.

US residency or a visa. Property ownership has no immigration component. You can own and close on US real estate without ever entering the country.

A US personal address. Your LLC’s registered agent address handles this. Wyoming and Delaware registered agent services run about $50–100/year.

To physically visit the property. I’ve closed 24 deals. I’ve never walked through most of what I own. You handle the physical inspection via your local team — investor-friendly agent, property manager, contractor. They’re your eyes on the ground.

The Sequence Matters More Than the List

Most foreign nationals find a deal first, then scramble to figure out the structure. By the time they get a property under contract, they have no LLC, no bank account, and no way to wire a down payment. The deal dies.

The right approach: build the infrastructure before you need it.

Form your LLC → apply for your EIN simultaneously → start your ITIN application immediately → open the US bank account once you have LLC docs and EIN → get DSCR pre-qualified.

Then look at deals.

The ITIN Problem

The ITIN is the one that catches people. Six to eleven weeks is the IRS’s processing time for Form W-7. That’s not business days — that’s weeks. If you apply for your ITIN after you find a deal, there’s a real chance you won’t have it before you need to close. Some lenders will work around this; most won’t.

The fix: apply for your ITIN the week your LLC is formed. By the time you’ve done your market research, built your local team, and found a deal worth making an offer on — your ITIN will be in hand.

For the application, you’ll need Form W-7 and either your original passport or a certified copy from your home country’s embassy or consulate. The IRS accepts applications by mail or through an IRS-authorized Acceptance Agent — typically a US CPA or tax attorney who handles non-resident clients.

How Financing Works for Foreign Nationals

This is where most international investors assume the door is closed. It isn’t.

What doesn’t work: conventional mortgages. Those require a Social Security number, US credit history, and W-2 income documentation. They’re built for US residents.

What works: DSCR loans. Debt Service Coverage Ratio lending qualifies on the property’s income, not yours. The lender asks one question: does the monthly rent cover the mortgage payment?

The ratio they look for is typically 1.0–1.25x. If the property rents for $1,500 and the PITI (principal, interest, taxes, insurance) is $1,200, your DSCR is 1.25. Most lenders will fund that.

As a foreign national, expect to put 25–30% down. The loan goes in your LLC’s name, not yours personally. The lender will want your ITIN, LLC documents, proof of funds for the down payment, and a signed lease or a market rent analysis.

My second BRRRR deal — Fayetteville, NC, 2021 — was financed with a DSCR loan. The loan was in the LLC’s name. It closed with a wire transfer from my Mercury business account. I was in Tel Aviv. The lender never asked for my personal income because the property proved it for me: $1,400/month rent against a $1,050 PITI. Done.

If you want the full mechanics of how DSCR loans work for foreign nationals — including the questions to ask lenders before applying — that’s covered in DSCR Loans for Non-US Citizens.

What the Setup Actually Costs

One-time costs, roughly:

- LLC formation: $300–500 (Wyoming or Delaware; use a registered agent service)

- EIN: Free if you apply yourself; $150–300 if using a formation service

- ITIN: Free via Form W-7 (budget $50–150 for certified document copies)

- US bank account: Free — Mercury and Relay have no monthly fees for basic accounts

- CPA (first-year setup): $1,500–3,000 — necessary for your first US tax filing and entity structure review

- DSCR loan origination: 1–2% of the loan amount at closing — not upfront

Total before your first deal: roughly $2,000–5,000. That’s a one-time setup for an infrastructure that serves your entire portfolio. My entity structure is still the same one I set up in 2020. I’ve put 24 deals through it.

The Common Mistakes

Forming the LLC in the investment state. Don’t. Wyoming and Delaware give you better asset protection and are built for exactly this use case. Register the LLC as a foreign entity in your investment state separately if required — usually a $100–300 filing.

Starting the ITIN after you find a deal. Already covered. Do it when you form the LLC.

Making offers before you have a bank account. You can’t wire a deposit from a foreign personal account without international wire complications. Have the US business account funded and ready before you’re in contract.

Buying without a property manager in place. You’re investing remotely. You need boots on the ground before you own something. Vet the PM before you buy, not after.

Working with a general real estate agent instead of an investor-friendly one. Most agents don’t understand ARV, BRRRR, or how to evaluate a value-add deal. Find someone who works with investors and knows the local rental market.

The full framework for how to build this team before you buy — agent, PM, contractor — is in How to Invest in US Real Estate from Abroad.

Frequently Asked Questions

Can a non-resident alien buy property in the US?

Yes. Non-resident aliens have the same property ownership rights as US citizens for investment property. There are no federal restrictions on foreign national ownership of US real estate.

Do I need a US visa to buy property?

No. Real estate ownership has no immigration component. You can own, close on, and collect rent from US property without ever entering the country.

What taxes do I pay as a foreign national landlord?

Non-residents default to 30% withholding on gross rental income. Most investors elect to treat US rental income as effectively connected income (ECI), which lets you deduct operating expenses and pay tax on net income at ordinary rates — usually a much better outcome. Your US CPA makes this election on your first tax return. FIRPTA also applies when you eventually sell — worth understanding before you buy, not after.

Can I get a mortgage as a foreign national?

Not a conventional mortgage — those require a Social Security number and US credit history. But DSCR loans are widely available to foreign nationals. No SSN, no US credit history, no W-2 required. You need an ITIN, an LLC, a qualifying property, and 25–30% down.

What state should I form my LLC in?

Wyoming is the most common choice for foreign national investors — strong asset protection, no state income tax, minimal filing requirements, low annual fees. Delaware is also widely used. Neither requires you to live or invest there.

Can I use my foreign income to qualify for a loan?

For DSCR loans, it doesn’t matter — the loan qualifies on the property’s income, not yours. For other loan types, foreign income documentation is complex and most lenders won’t touch it. Stick to DSCR for investment property financing as a foreign national.

If you’re starting from scratch and want a clear sequence of steps — entity setup, financing, team, and first deal — I put that together in the Remote Investor First Deal Roadmap. It’s the practical companion to this post.

Find out exactly where you stand before your first deal.

10 questions. A personalized score across 5 dimensions. Free.

Get my readiness score →