Key Takeaways

- DSCR loans are the only realistic financing path for foreign nationals buying US investment property

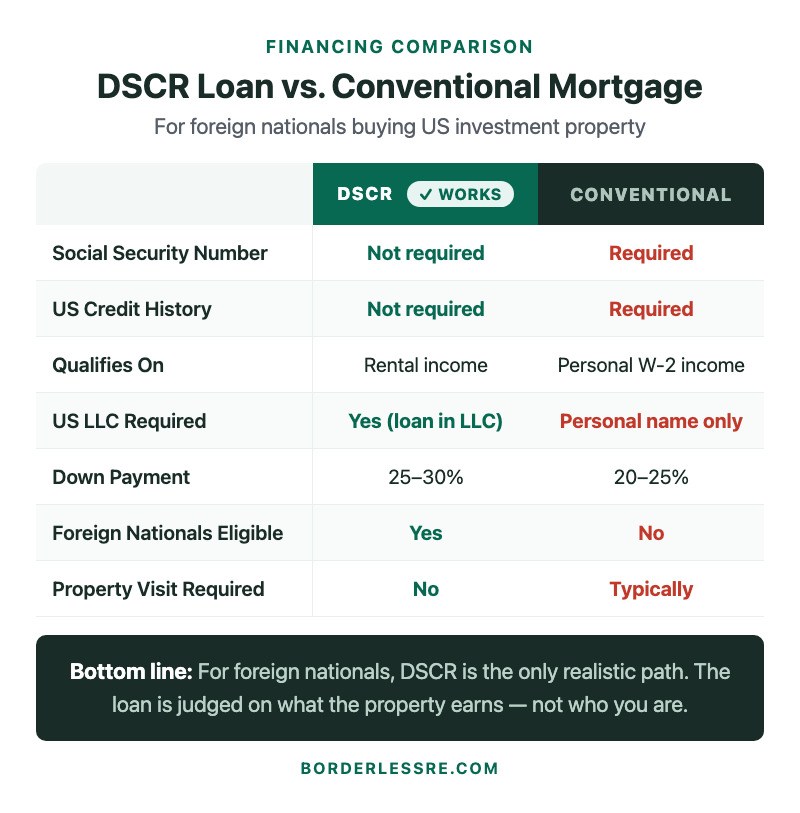

- They qualify on the property’s rental income — not your personal income, credit score, or country of residence

- You need an ITIN, a US LLC, 25–30% down, and a property whose rent covers the payment at a 1.0–1.25x ratio

- No US Social Security number, no US credit history, no W-2 required

- Get pre-qualified before you’re under contract — not after. Know your rate and down payment requirement first.

- The appraisal and entire process can be done without visiting the property

IN THIS ARTICLE

Every article about DSCR loans for foreign nationals is written by a lender explaining their product.

This one is written by a borrower who has used them. Multiple times. From Israel.

I’ve financed US investment properties with DSCR loans without a US Social Security number, without US credit history, and without visiting most of the properties. The math is simple. The process is learnable. And if you’re a foreign national trying to buy US investment property, this is the only financing vehicle that was actually built for your situation.

Here’s what the lender websites won’t tell you.

What Is a DSCR Loan (From a Borrower’s View)

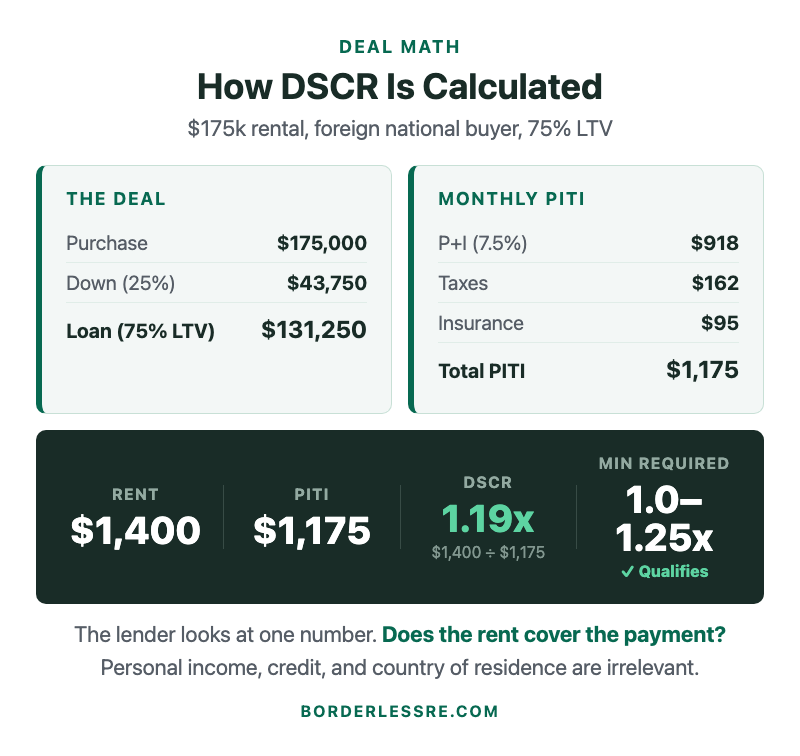

DSCR stands for Debt Service Coverage Ratio. The ratio is: monthly rent divided by monthly PITI (principal, interest, taxes, insurance).

That’s the entire qualification engine. The lender looks at that one number and asks: does this property’s income cover its own debt? If yes — and the ratio hits their minimum, typically 1.0 to 1.25x — the loan gets done.

What makes DSCR different from every other mortgage product: your personal income, employment history, credit score, and country of residence are not part of the underwriting. The property qualifies, not you. That’s not a workaround — that’s how the product was designed.

DSCR loans are non-QM (non-qualified mortgage) products. They sit outside the Fannie Mae / Freddie Mac framework, which is why they can skip the W-2 and credit score requirements. They’re funded by private capital and portfolio lenders, and the rates reflect that — typically 0.5–1.5% above conventional rates, depending on the lender and the deal.

How DSCR Works Differently for Foreign Nationals

The core mechanics are the same. The foreign national wrapper adds a few requirements and removes a few options.

The key differences for foreign nationals:

The loan goes in your LLC’s name, not yours. This is standard for DSCR foreign national loans. Your US LLC is the borrower of record. You sign as the guarantor. This is actually an asset protection feature, not just a requirement.

You need an ITIN, not an SSN. The ITIN (Individual Taxpayer Identification Number) is what most DSCR lenders require from non-resident foreign nationals. This matters because ITINs take 6–11 weeks to process — if you don’t already have one, start the application before you start shopping for deals. I’ve seen investors lose properties because they applied for the ITIN after they were under contract.

Down payment is 25–30%. Domestic investors can sometimes get DSCR loans at 20% down. Foreign nationals almost universally land at 25–30%. Budget for 25% minimum; confirm the requirement with each lender before applying.

Some lenders won’t touch foreign national loans at all. The DSCR market is large, but not every lender is set up for non-resident borrowers. Ask the question in your first conversation: “Do you do foreign national DSCR loans for non-resident borrowers without a US SSN?” If they hesitate, move on. There are enough lenders who do this regularly that you don’t need to educate someone doing it for the first time.

The Math: How the Ratio Is Calculated

The ratio is simple. What trips people up is understanding exactly what goes into the denominator.

PITI = Principal + Interest + Taxes + Insurance. The lender uses the full monthly payment, not just principal and interest. This is the number that catches investors off guard — they run the math on PI only, the deal looks great, then the lender includes taxes and insurance and the ratio drops below their minimum.

Some lenders also include HOA fees in the denominator if the property is in an HOA. Always ask what’s included in their DSCR calculation before you underwrite a deal against their minimum.

On the rent side: if the property is already leased, most lenders use the actual lease amount. If it’s vacant, they use a market rent appraisal — typically ordered as part of the appraisal process. The appraiser will comp rental rates in the market and give the lender a market rent figure. That’s what gets used to calculate the ratio on a vacant property.

My Fayetteville BRRRR deal: $102k purchase, $18k rehab, refinanced at 75% LTV on a $165k appraisal = $123,750 loan. Monthly PITI came to roughly $1,050. Property was already leased at $1,400/month. DSCR: 1.33x. The loan closed from 7,000 miles away. I never saw the appraiser. My property manager let them in.

What You Actually Need to Qualify

The short list:

- US LLC — the loan entity. Wyoming or Delaware formation, registered as a foreign entity in your investment state if required.

- ITIN — your individual US tax ID. Start the application early. Most lenders require it; a few will work with it pending but confirm before applying.

- 25–30% down payment — wired from your US business bank account. Lenders want to see the funds in a US account, not an international transfer landing on closing day.

- Proof of funds — typically 2–3 months of bank statements showing you have the down payment plus reserves (usually 6 months of PITI in reserve post-closing).

- A qualifying property — rent-to-PITI ratio at or above the lender’s minimum. Most require 1.0–1.25x. Some will go to 0.75x for strong borrowers (called “no-ratio” DSCR), but expect a higher rate.

- A signed lease or market rent appraisal — establishes the rent figure used in the ratio. If the property is already tenanted, your lease does this. If vacant, the appraiser comps it.

What you don’t need: W-2 income, tax returns, US credit score, pay stubs, US employment history. None of it. The underwriting is entirely property-based.

The Application Process — Done Remotely

The DSCR application process is more straightforward than a conventional mortgage, and it can be done entirely remotely. Here’s the typical sequence:

Pre-qualification (before you’re under contract). Share your LLC docs, ITIN, proof of funds, and the general deal parameters (purchase price, estimated rent, target LTV). The lender gives you a rate quote and confirms the down payment requirement. This takes 1–3 business days.

Full application (once you’re under contract). The property address is now confirmed. The lender orders the appraisal — which includes the market rent analysis if the property is vacant. You submit your LLC operating agreement, proof of funds, and sign the application documents electronically.

Appraisal. A licensed appraiser inspects the property and produces a report that includes both the fair market value and a market rent estimate. Your property manager or agent coordinates access. You don’t attend. I’ve never attended an appraisal.

Underwriting and closing. Once the appraisal is in and the DSCR ratio is confirmed, underwriting is usually 2–3 weeks. Closing documents are sent electronically or via overnight courier to wherever you are. Wire the down payment from your US business account. Done.

Total timeline from application to close: typically 30–45 days. Some lenders move faster. Build your contract closing period around this — 30 days is tight, 45 is comfortable.

Questions to Ask Lenders Before Applying

This is the part lender websites never cover. These questions save you weeks of wasted time.

“Do you do DSCR loans for non-resident foreign nationals without a US SSN?” Ask this first. Some lenders say yes to DSCR and no to foreign nationals. Get clarity before you fill out an application.

“What is your minimum DSCR ratio?” Varies by lender. Most are 1.0–1.25x. Some have no-ratio products at 0.75x or below at higher rates. Know the threshold before you underwrite a deal to their requirements.

“What goes into your DSCR denominator — is it PITI, or do you include HOA?” Some lenders include HOA fees. Others don’t. A $300/month HOA on a $1,400 rent property changes your ratio materially.

“Do you accept a pending ITIN, or must it be issued?” If your ITIN application is still in process, some lenders will proceed with a commitment letter; others won’t fund until it’s issued. Know this before you sign a contract.

“What reserves do you require post-closing?” Standard is 6 months of PITI in reserves after the down payment. Some require 12. Your proof of funds needs to cover both.

“What states do you lend in?” Not all DSCR lenders are licensed in every state. Confirm your investment state is covered before going further.

Common Pitfalls

Getting under contract before pre-qualifying. You don’t know your actual rate or down payment requirement until a lender confirms it. Running a deal analysis with assumed numbers, then discovering the reality is 0.5% higher on rate and 5% higher on down payment, can kill a deal that looked profitable on paper.

Using estimated taxes and insurance in your DSCR calculation, not actual. Tax estimates from Zillow or Redfin are often wrong — especially in states where property taxes reset on sale. Get the actual current tax bill from county records, and get a real insurance quote before underwriting the deal. I’ve seen deals fail DSCR after closing because taxes were 40% higher than the Zillow estimate.

Wiring the down payment from a foreign account at closing. Some lenders and title companies flag international wires as suspicious, creating delays. Have your US business account funded and ready well before closing. Wire domestically.

Applying to a lender who has never done a foreign national DSCR loan. They’ll say yes, waste 3 weeks of your time, then come back with issues at underwriting. Ask for their foreign national experience upfront. Ask if they have a specific foreign national loan program or if they’re trying to adapt a domestic one.

Not leaving enough time for the appraisal. Appraisals can take 2–3 weeks in some markets. In rural or low-inventory markets, finding a licensed appraiser familiar with the local comps can add another week. Budget for this in your contract period.

Frequently Asked Questions

Can a foreign national get a DSCR loan?

Yes. DSCR loans are one of the few mortgage products explicitly designed for non-resident foreign nationals. They don’t require a US Social Security number, US credit history, or W-2 income. The property’s rental income is what qualifies the loan.

What credit score do I need for a DSCR loan as a foreign national?

Most foreign national DSCR programs don’t require a US credit score at all — because foreign nationals don’t have one. Some lenders will pull an international credit report; others simply don’t require it. Confirm with each lender how they handle this. It’s usually not a barrier.

How much do I need to put down on a DSCR loan?

As a foreign national, expect 25–30% down. Some lenders will go to 25% on a purchase; refinances at 75% LTV are more common for BRRRR deals. Confirm the exact requirement before you underwrite a deal — and make sure your proof of funds covers the down payment plus 6 months of post-closing reserves.

Do I need to visit the property to get a DSCR loan?

No. The lender sends an appraiser; your local contact (agent or property manager) provides access. All documents are signed electronically. The down payment is wired. You don’t need to be there — or even in the country.

What is a good DSCR ratio?

1.25x or above is comfortable and qualifies with almost any lender. 1.0–1.25x qualifies with most. Below 1.0x (meaning the rent doesn’t fully cover the payment) is possible with some “no-ratio” DSCR products but comes with a higher rate and stricter terms. Target 1.2x or above when underwriting a deal — it gives you margin if taxes or insurance come in higher than expected.

Can I use a DSCR loan for a BRRRR deal?

Yes — this is exactly what DSCR loans are built for in the BRRRR context. You buy with cash (or hard money), rehab, lease, then do a DSCR cash-out refinance based on the after-repair appraised value. The refinance pays back some or all of your original capital, and the remaining loan qualifies on the new rental income. That’s the exact structure I used in Fayetteville.

The setup that makes all of this possible — LLC, ITIN, US bank account, and DSCR pre-qualification — is covered step by step in Can a Non-US Citizen Buy Investment Property in the USA? and in the broader practitioner’s guide to investing from abroad.

If you want to know where you actually stand on financing access before you start approaching lenders, the Remote Investor Readiness Score walks through the financing dimension specifically — what you have, what’s missing, and what to do first.

Find out exactly where you stand before your first deal.

10 questions. A personalized score across 5 dimensions. Free.

Get my readiness score →